Daily Analysis 20231023

Oct 23rd, 2023

Good morning,

Dow closes nearly 300 points lower after 10-year Treasury yield tops 5% for the first time since 2007

Stocks retreated Friday as a surge in the 10-year Treasury yield

prompted broader concerns about the state of the economy.

Dow……33127 -286.9 -0.86%

Nasdaq12984 -202.4 -1.53%

S&P 500.4224 -53.8 -1.26%

FTSE…..7402 -97.4 -1.30%

Dax……14798 -246.8 -1.64%

CAC……6816 -105.2 -1.52%

Nikkei…31259 -171.3 -0.54%

HSI…….17172 -123.8 -0.72%

Shanghai.2983 -22.3 -0.74%

IDX….6849.17 +2.74 +0.34%

LQ45….911.89 +1.81 +0.20%

IDX30…470.40 +0.82 +0.17%

IDXEnergy..2076.00 +1.39 +0.07%

IDX BscMat.1242.30 +0.85 +0.07%

IDX Indstrl…1122.38 +0.16 +0.01%

IDXNONCYC.745.20 +0.38 +0.05%

IDX Hlthcare1484.38+3.41 +0.23%

IDXCYCLIC…853.51 -1.83 -0.21%

IDX Techno.3949.22 -66.56 -1.66%

IDX Transp 1683.76 -28.25 -1.65%

IDX Infrast..1215.98 -9.97 -0.81%

IDX Finance.1356.92 +1.85 +0.14%

IDX Banking.1174.98 +10.95+0.94%

IDX Property…698 -5.40 -0.77%

Indo10Yr.7.1419‼ +0.1088+1.55%

ICBI….361.0366‼-2.0354 -0.56%

US2Yr.5.071‼ -0.038 -0.74%

US5Yr 4.854 -0.100 -2.02%

US10Yr4.914 -0.081 -1.62%

US30Yr.5.078‼ -0.031 -0.61%

VIX…..21.71‼ +0.31 +1.45%

USDIndx 106.1630‼-0.090 -0.08%

Como Indx…286.01 -1.32 -0.46%

(Core Commodity CRB)

BCOMIN…..136.16 -0.26 -0.19%

IndoCDS.102.96 +2.96 +2.96%‼

(5-yr INOCD5) (20/10)

IDR…..15872.50‼ +57.50 +0.36%

Jisdor.15856.00‼ +18.00 +0.11%

Euro……1.0594 +0.0014 +0.13%

TLKM…23.53 -0.16 -0.68%

(3731)

EIDO….20.92 +0.08 +0.38%

EEM….36.79 -0.45 -1.21%

Oil………88.08‼ -2.26 -2.50%

Gold..1994.40‼ +8.00 +0.40%

Timah..24985.00 -220.00 -0.97%

(Closed 20/10)

Nickel..18648.00 +91.00 +0.49%

(Closed 20/10)

Silver……23.50 +0.35 +1.51%

Copper.356.30 -2.05 -0.57%

Iron Ore 62%118.65 -0.39 -0.33%

(20/10)

Nturl Gas…3.258 +0.303 +10.25%‼

Ammonia China.3700.00 +76.67 +2.12%

(Domestic Price)(19/10)

Coal price.138.00 +1.50 +1.10%

(Oct/Newcastle)

Coal price.143.00 +1.00 +0.70%

(Nov/Newcastle)

Coal price.145.40 -0.60 -0.41%

(Des/Newcastle)

Coal price 150.50 -0.45 -0.30%

(Jan/Newcastle)

Coal price.138.00 +0.50 +0.36%

(Oct/Rotterdam)

Coal price.139.10 +1.00 +0.73%

(Nov/Rotterdam)

Coal price.136.90 -0.10 -0.07%

(Des/Rotterdam)

Coal price 136.20 -0.05 -0.04%

(Jan/Rotterdam)

CPO(Jan)..3771 +25 +0.67%

(Source: bursamalaysia.com)

Corn……495.00 -9.50 -1.88%

SoybeanOil 53.39 +0.28 +0.53%

Wheat….586.00 -8.00 -1.35%

Wood pulp..5700.00 -10 -0.18%

(Closed 22/10)

©Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia.

Copyright: Phintraco Sekuritas

Jum’at kebakaran semua, bagusnya sih US Bond rate turun, harusnya dampaknya bagus ke saham, USD index turun, Gold silver naik, copper timah nickel iron ore turun, oil turun, gas loncat, Coal tipis2, spot ijo future merah. Harusnya bagus buat ANTM MDKA dan saham2 tambang batubara. PGAS sayangnya ga selalu sejalan sama harga gas, jadi walau loncat ga banyak ngaruh

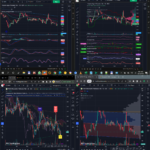

IHSG – ga jadi buy MACD nya, stoch nya ngebalik sell, masih FNS terus, masih distribusi terus, bikin lower low,jadi terbuka kemungkinan ABC correction nya bukan kaya yang kemaren digambar, tapi di 6750 an targetnya. Masih bagus pegang cash…

Energy, Infrastructure

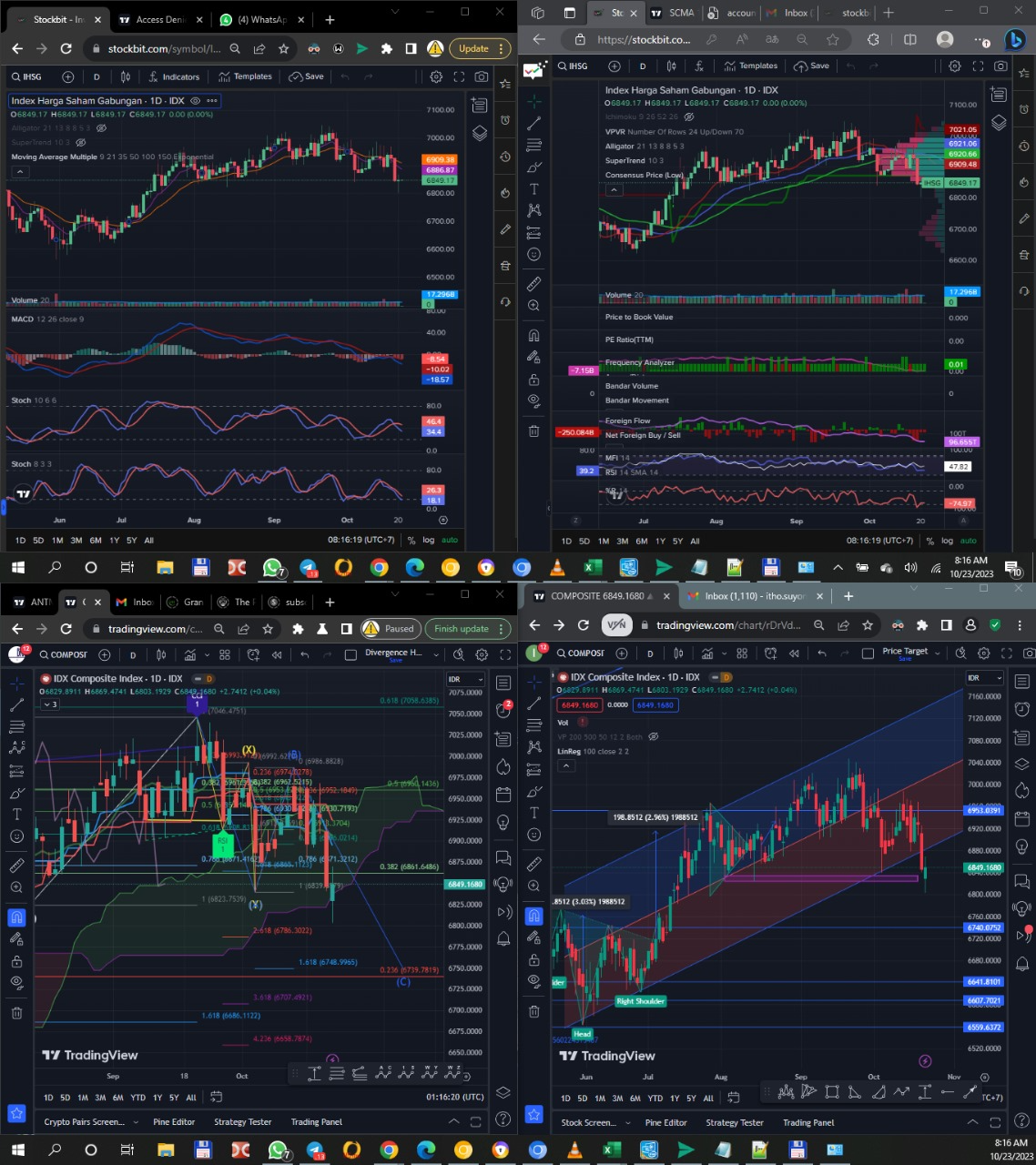

Stochastic Buy Signal: ICBP AALI TAPG

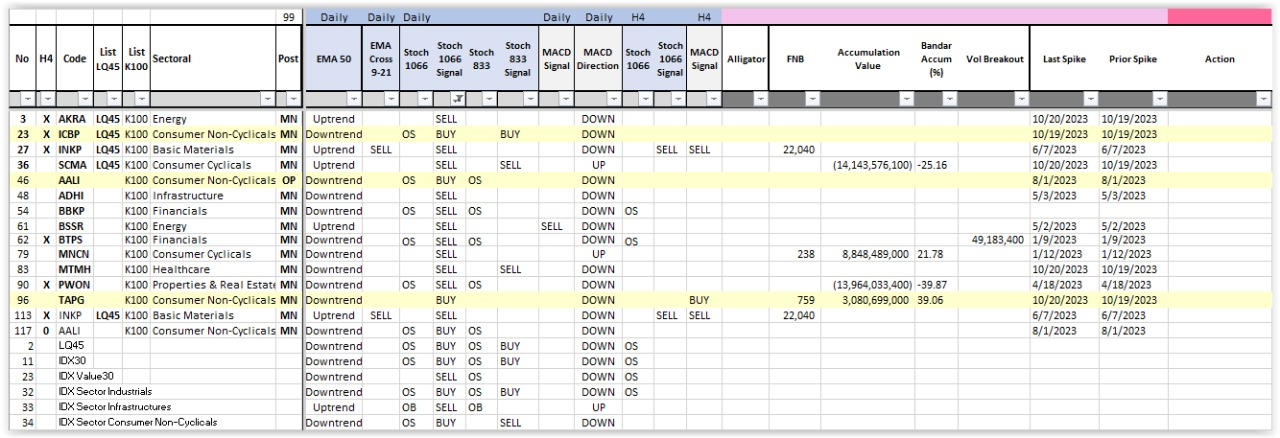

MACD Buy Signal: HRUM BRMS

Stochastic Continuation Signal: SIDO BMTR HMSP LPPF

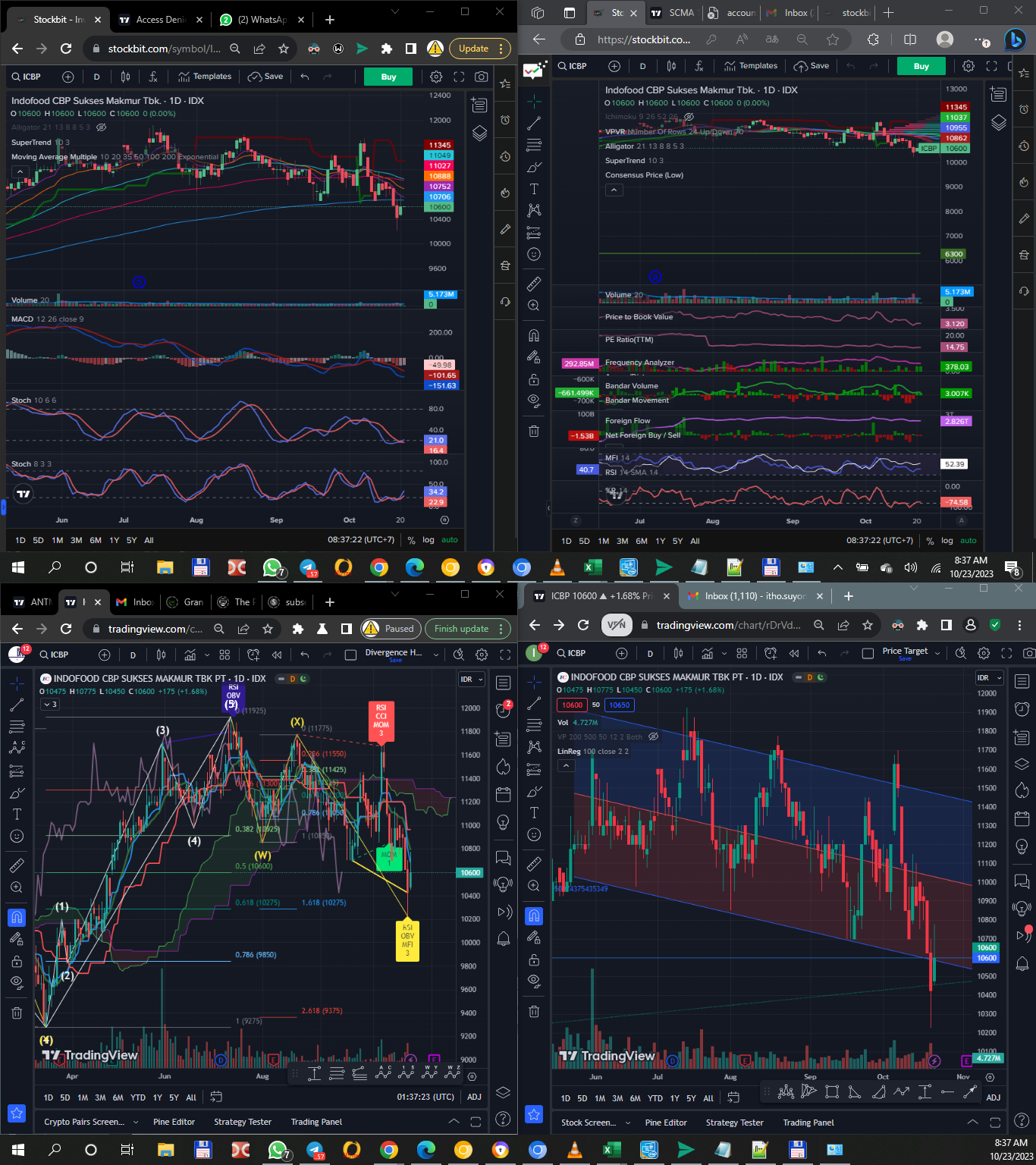

ICBP – stoch buy macd down, MFI sw, w% baru keluar downtrend area, BD rev acc, FF masih dist, abis wave 5 udah bikin abc correction,udah kemu reg bull div, baru satu cendol. Wait confirmation…

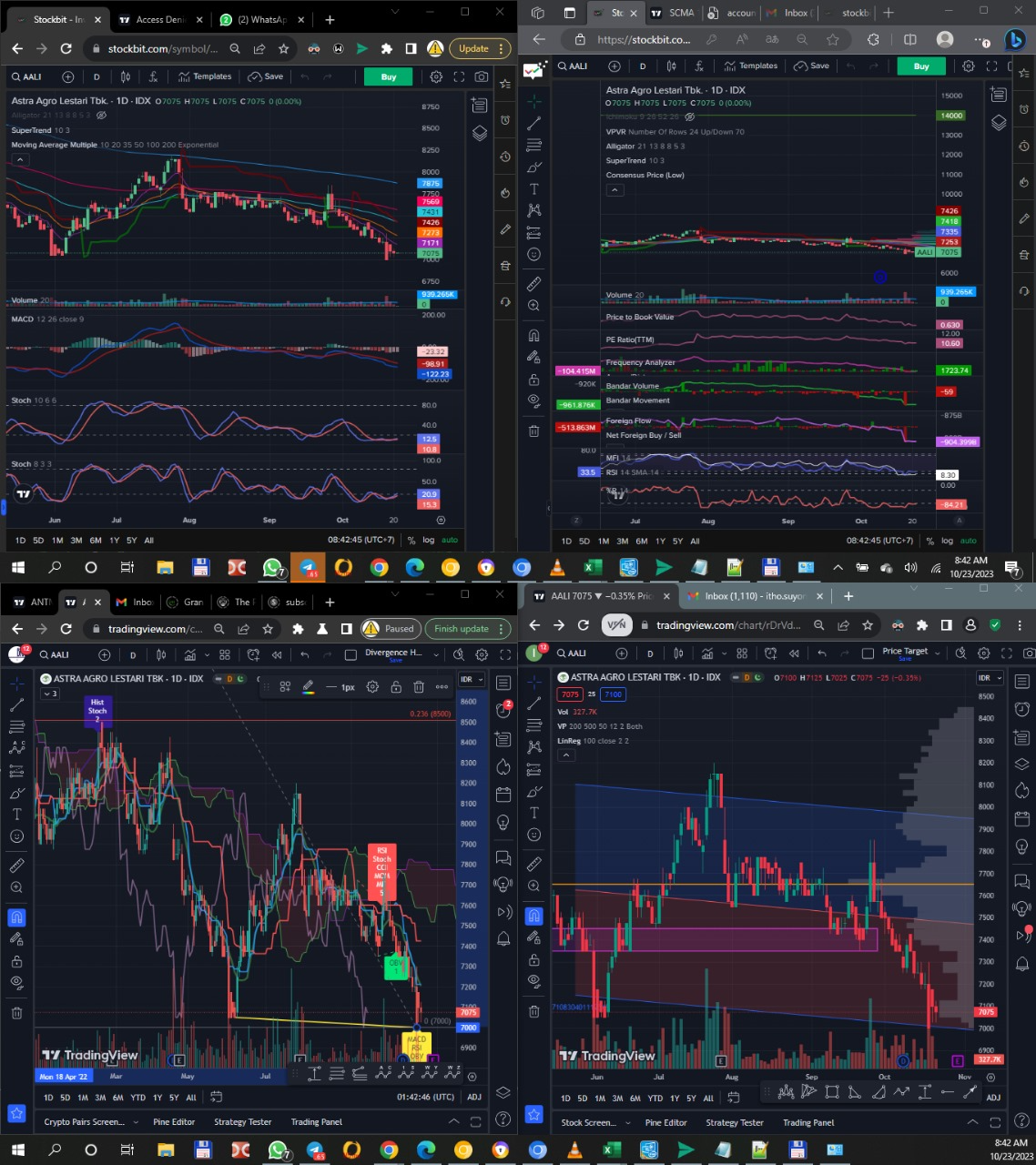

AALI – masih jelek semua kecuali stochastic buy dan ketemu reg bull div, tunggu confirm

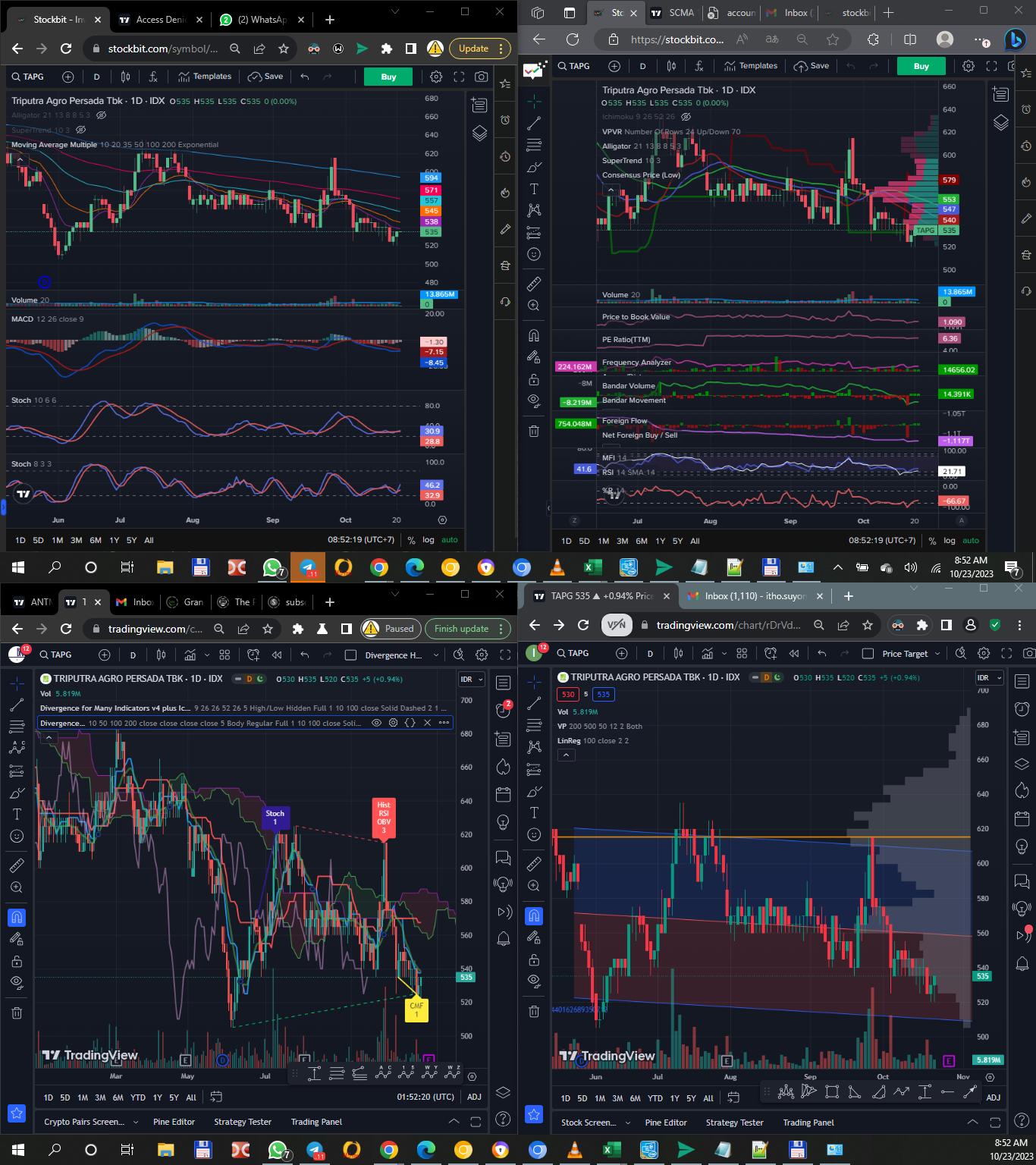

TAPG – lebih bagus technicalnya, stoch buy, macd rev up, w% up, BD FF rev acc, bikin higher low, ada reg bear div di chaikin money index, tapi belum berani entry, macd buy signal kita assess lagi