Daily Analysis 20240117

January 17th, 2024

Good morning,

Dow closes more than 200 points lower Tuesday after 10-year Treasury yield tops 4%

The Dow Jones Industrial Average fell Tuesday as bond yields ticked higher and Wall Street pored through the latest batch of fourth-quarter earnings.

Dow……37361 -231.9 -0.62%

Nasdaq14944 -28.4 -0.19%

S&P 500.4766 -17.9 -0.37%

FTSE…..7558 -36.6 -0.48%

Dax……16572 -50.5 -0.30%

CAC……7398 -13.7 -0.18%

Nikkei..35619 -15.42 -0.78%

HSI…….15866 -350.4 -2.16%

Shanghai.2894 +7.7 +0.27%

IDX…..7242.79 +18.70 +0.26%

LQ45….975.39 +1.34 +0.14%

IDX30…502.80 -0.35 -0.07%

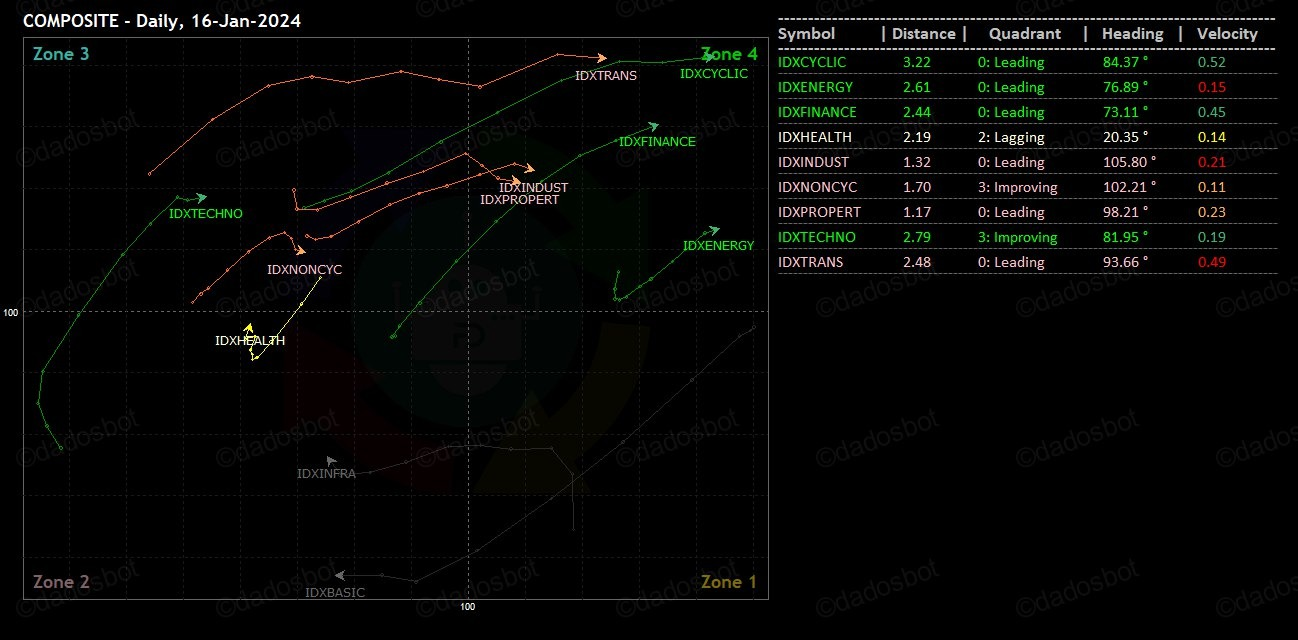

IDXEnergy..2194.91 .91 +1.06%

IDX BscMat.1249.83 +0.41 +0.03%

IDX Indstrl…1127.74 +11.77+1.06%

IDXNONCYC.707.91 +1.34 +0.19%

IDX Hlthcare1310.72 -25.74 -1.93%

IDXCYCLIC…864.61 +8.98 +1.05%

IDX Techno4310.93 -26.38 -0.61%

IDX Transp 1710.92 -0.81 -0.05%

IDX Infrast 1534.48 +2.42 +0.16%

IDX Finance.1512.23 -4.22 -0.28%

IDX Banking.1331.17 -1.46 -0.11%

IDX Property.. 714 +1.40 +0.19%

Indo10Yr.6.6805 +0.0229 +0.34%

ICBI…375.0189 +0.0247 -0.01%

US2Yr.4.222 +0.076 +1.83%

US5Yr 3.934 +0.102 +2.66%

US10Yr4.064 +0.078 +1.96%

US30Yr.4.297 +0.122 +2.92%

VIX….13.84 +0.59 +4.45%‼️

USDIndx 103.3570❗️ +0.953 +0.93%

Como Indx..264.30 -0.08 -0.03%

BCOMIN……136.24 +0.24 +1.29%

IndoCDS..74.21 -0.02 -%

(5-yr INOCD5) (12/01)

IDR…..15592.50 +37.50 +0.24%

Jisdor.15592.00 +37.00 +0.24%

Euro….1.0877 -0.0072 -0.66%

TLKM…25.80 -0.12 -0.43%

(4033)

EIDO……22.44 -0.21 -0.93%

EEM……38.25 -0.95 -2.42%

Oil……..72.40 -0.10 -0.14%

Gold..2030.20 -28.80 -1.40%

Timah..24781.00 +150.00 +0.61%

(Closed 15/01)

Nickel..16227.00 +59.5 +0.37%

(Closed 16/01)

Silver……23.09 -0.24 -1.01%

Copper.376.65 -1.75 -0.46%

Iron Ore 62% 137.22 – -%

(12/01)

Nturl Gas..2.829 -0.277 -8.92%‼️

Ammonia China.3183.33‼️ -66.67 -2.05%

(Domestic Price)(15/02)

Coal price.129.50 -0.35 -0.39%

(Jan/Newcastle)

Coal price 127.40 +1.15 +0.91%

(Feb/Newcastle)

Coal price.127.25: +1.00 +0.80%

(Mar/Newcastle)

Coal price 125.85 +0.85 +0.68%

(Apr/Newcastle)

Coal price.107.75 +0.25 +0.23%

(Jan/Rotterdam)

Coal price 103.75 +2.25 +2.22%

(Feb/Rotterdam).

Coal price..100.85 +1.80 +1.82%

(Mar/Rotterdam)

Coal price…99.30 +1.80 +1.85%

(Apr/Rotterdam)

CPO(Apr)..3881 +61 +1.61%

(Source: bursamalaysia.com)

Corn……443.50 -3.50 -0.78%

SoybeanOil 48.25 -1.00 -2.07%

Wheat…582.00 -14.00 -2.35%

Wood pulp..5054.00+4.00 +0.10%

(Closed 16/01)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

Weh, US lanjut merah, europe juga, asia cenderung merah, yang ijo tipis. IHSG kemaren ijo, jadi kemungkinan merah lagi hari ini.

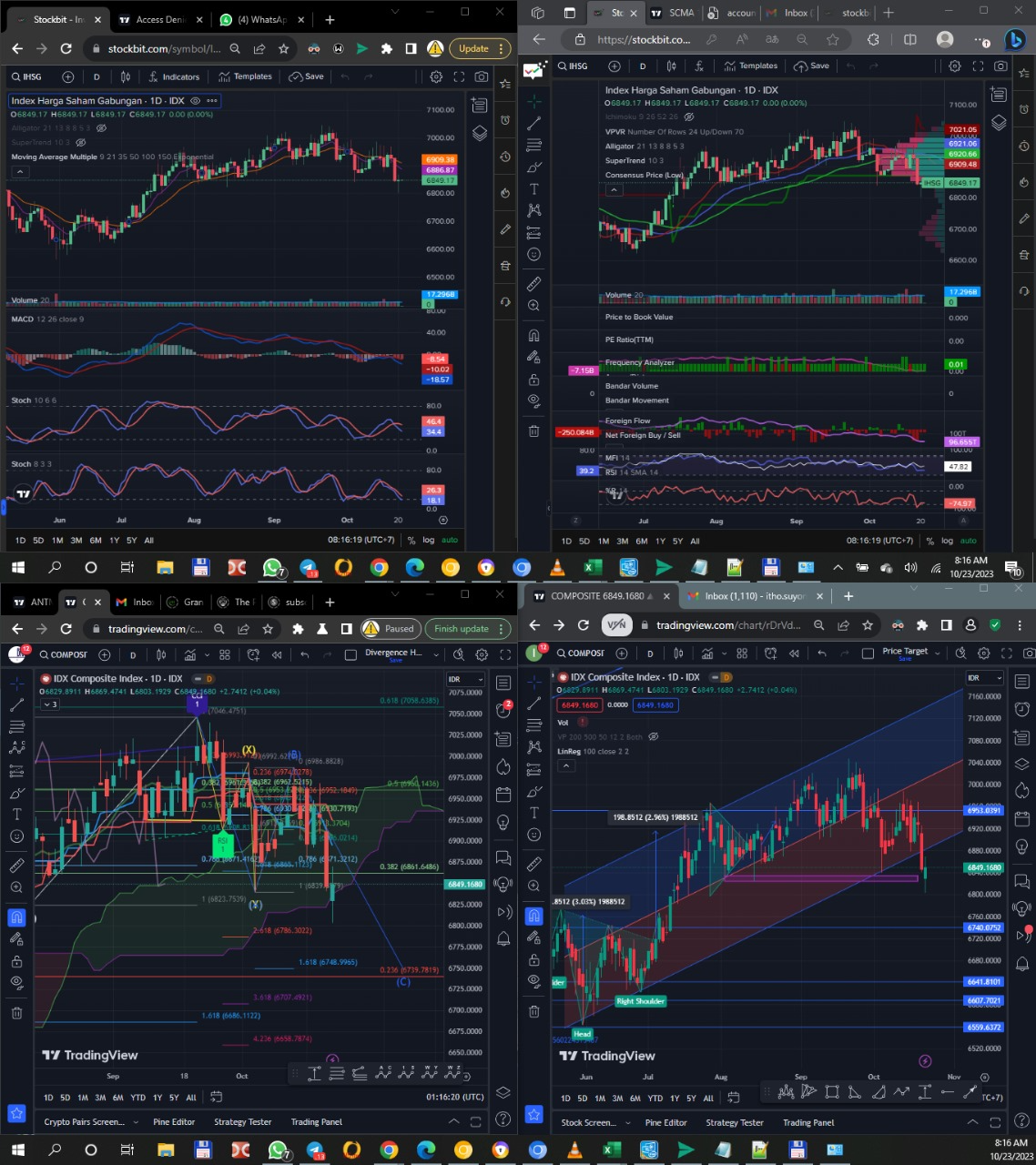

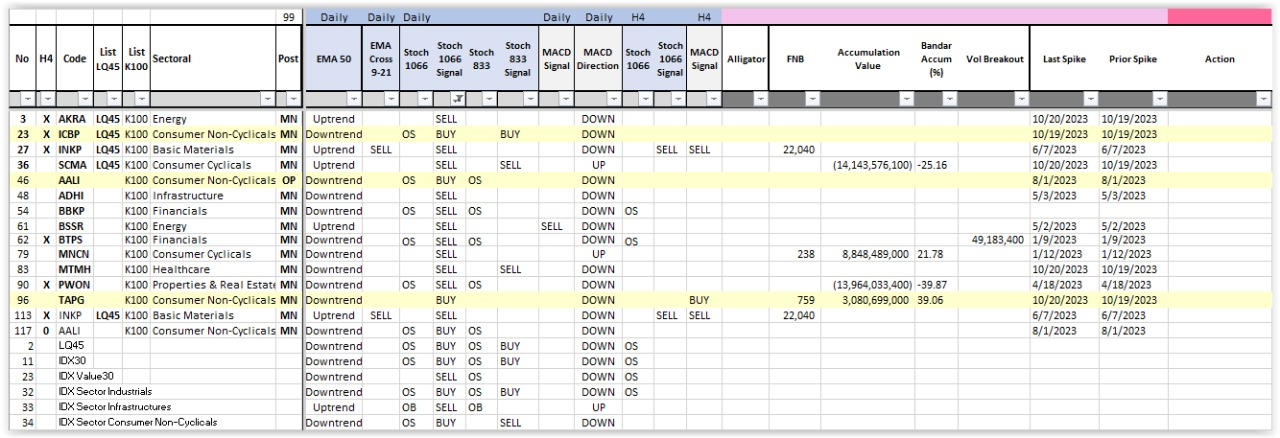

US Bond rate up rada tingi, bad for stocks, USD index juga naik, bad for commodities in general. Kebanyakan metal down kecuali Tin and Nickel, Oil down, Gas Drop, tapi Coal and CPO up. Good for ADRO PTBA ITMG INDY AALI LSIP

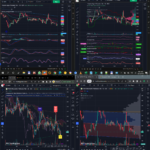

IHSG – stoch down macd down MFI sw, w% sw, BD sw, FNB, hidden bullish divergence, 833 buy, semoga rada ada dorongannya minimal ga dibanting, sideways correction aja

Still financials, energy, yang ketangkep kemaren beli KLBF ini mulai keliatan healthcare mau bangun. Property yang kayanya udahan