Daily Analysis 20220825

Global update:

August 25th, 2022

Good morning,

Stocks end Wednesday higher, Dow and S&P 500 snap three-day slide

Stocks rose Wednesday, snapping a three-day decline in the Dow and the S&P 500, as investors awaited more clarity on the Federal Reserve’s fight against inflation.

Dow…….32969 +59.6 +0.18%

Nasdaq.12432 +50.2 +0.41%

S&P 500..4141 +12 +0.29%

FTSE…….7471 -16.6 -0.22%

Dax……..13220 +25.8 +0.39%

CAC……..6387 +24.7 +0.39%

Nikkei….28313 -139.3 -0.49%

HSI……..19269 -234.5 -1.20%

Shanghai..3215 -61.02 -1.86%

ST Times..3233 -12.7 -0.39%

IDX…….7194.71 +31.44 +0.44%

LQ45…1026.61 +3.61 +0.35%

IDX Energy…1859.83 +15.55 +0.84%

IDX Bsc Mat.1296.57 -4.59 -0.35%

IDX Industrl..1315.97 +10.02 +0.77%

IDXNONCYC..711.52 -2.66 -0.37%

IDX Hlthcare.1413.83 -0.05 -0.36%

IDXCYCLIC…..898.20 +0.81 +0.09%

IDX Techno..8058.64 +183.16 +2.33%

IDX Transp…2002.03 -8.51 -0.42%

IDX Infrast…..1038.90 +0.78 +0.07%

IDX Finance 1503.76 +2.60 +0.17%

IDX Banking..1138.23 -0.07 -0.01%

IDX Property…709 +2.04 +0.34%

Indo10Yr….7.1587 -0.0283 -0.39%

ICBI……..336.3387 +0.6148 +0.18%

US10Yr…..3.1060 +0.0520 +1.70%

VIX……….22.82 -1.29 -5.35%

USDIndx 108.6770 +0.0530 +0.05%

Como Indx..298.86 +2.55 +0.86%

(Core Commodity CRB)

BCOMIN…..156.83 -0.80 -0.51%

.

IndoCDS…110.95 – -%

(5-yr INOCD5)

IDR……14848.00 +10.50 +0.07%

Jisdor..14851 .00 -42.00 -0.28%

Euro………0.9969 -0.0001 -0.01%‼️

TLKM……..31.63 +0.55 +1.77%

(4697)

EIDO………23.92 +0.16 +0.67%

EEM………39.75 -0.01 -0.03%

Oil…………..95.25 +1.50 +1.60%

Gold ……..1764.40 +3.50 +0.20%

Timah. .24505.00 +40.00 +0.16%

( Closed 23/8)

Nickel….21407.50 -443.50 -2.03%‼️

(Closed 24/8)

Silver…….19.08 -0.02 -0.10%

Copper….364.50 -3.40 -0.92%

Nturl Gas…..9.236 -0.006 -0.06%

Ammonia….3733.33 unch +0%

China

(Domestic Price)(23/8)

Coal price….412.60 -5.00 -1.20%

(Agt/Newcastle)

Coal price….420.00 -5.00 -1.18%

(Sept/Newcastle)

Coal price….411.25 -8.75 -2.08%

(Okt/Newcastle)

Coal price….371.25 +1.25 +0.34%

(Agt/Rotterdam)

Coal price….376.90 -2.05 -0.54%

(Sept/ Rotterdam)

Coal price….368.40 -2.60 -0.70%

(Okt/Rotterdam)

CPO(Nov)……4304 +67 +1.58%

(Source: bursamalaysia.com)

Corn………..657.25 +2.00 +0.31%

SoybeanOil…65.98 -0.94 -1.40%

Wheat………813.25 +12.75 +1.59%

Wood pulp…6704.00 +4 +0.06%

(Closed 24/8)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

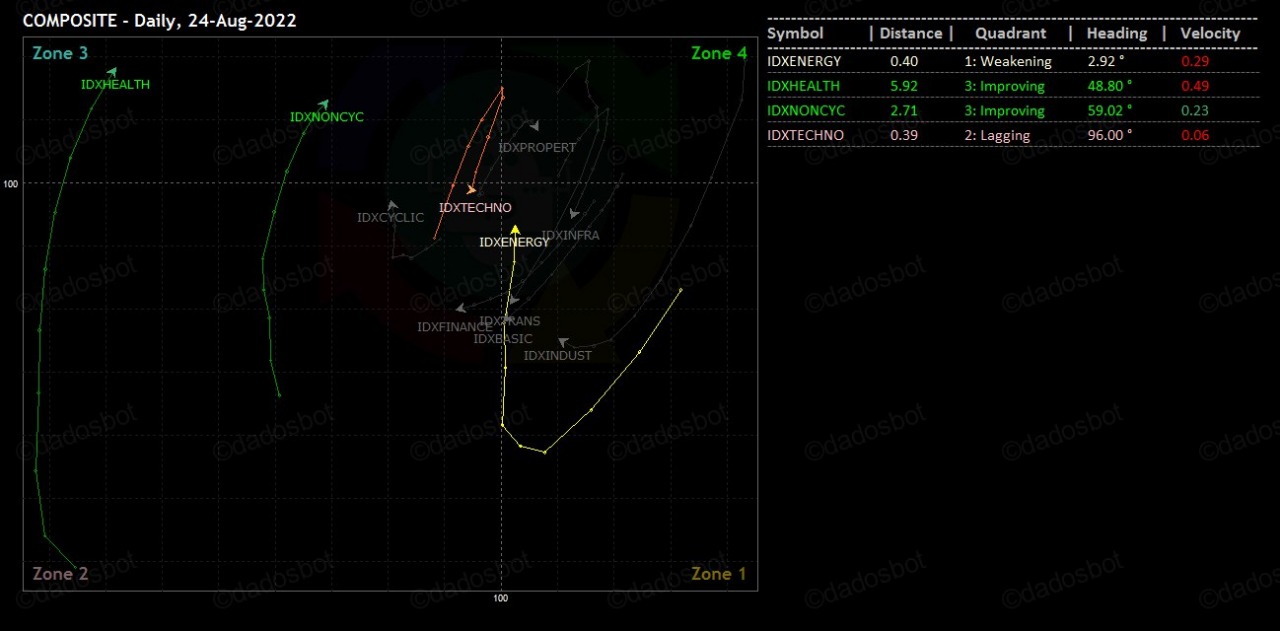

Nah, US ijo, IDX mau ikut ijo atau merah ya? Karena udah run 2 hari, kayanya opening ijo dulu terus closing merah. Yang pegang sektor non Energy Healthcare dan Consumer Non-cyclicals mending TP TP in dulu, minimal setengahnya

Europe mayoritas ijo, Asia mayoritas merah…

Oil Gold TImah CPO naik, Nikel Silver copper gas coal turun

Kesempatan ini buat BOW coal. CPO naik tapi ga terlalu significant kita coba liat efeknya ke AALI dan LSIP dari signal hari ini

IHSG – berhasil ijo lagi kemaren, disaat index regional lain pada merah. Di diskusi group2 wa dan telegram mulai keluar optimistic forecast: Mau bikin new All Time High… Bukannya ga ngarep itu kejadian, tapi index bikin new ATH itu harusnya gambaran dari keadaan ekonomi Indonesia, dan terpengaruh juga sama kondisi global. Kondisi ancaman perang dunia ke-4 dan krisis energi gini sepertinya sih bukan sentimen positif untuk sekarang2 bisa bikin new record high. Indicator2 technical nya juga kurang mendukung ke arah situ

Energy, Healthcare, Consumer Non-Cycicals, Technology

Energy – Still all good…

Kalopun turun keseret index aja keliatannya