Daily Analysis 20230228

February 28th, 2023

Good morning,

Stocks close higher following worst week of 2023, major indexes are on track to end February with declines

Stocks rose Monday as traders tried to recover some ground following the worst week of the year on Wall Street. Investors also looked ahead to another big week in retail earnings.

Dow…..32889 +72.2 +0.22%

Nasdaq11467 +72.04 +0.63%

S&P 500.3982 +12.2 +0.31%

FTSE…….7935 +56.5 +0.72%

Dax……..15381 +171.7 +1.13%

CAC……..7296 +108.3 +1.51%

Nikkei…..27424 -29.5. -0.11%

HSI………19944 -66.5 -0.33%

Shanghai.3258 -9.1 -0.28%

IDX…..6854.78 -1.8 -0.03%

LQ45….948.08 +1.15 +0.12%

IDX30…493.25 +0.92 +0.19%

IDXEnergy…2071.04 -1.47 -0.07%

IDX BscMat 1240.72 +2.34 +0.19%

IDX Indstrl…1158.68 +2.74 +0.24%

IDXNONCYC..746.74 -5.36 -0.71%

IDX Hlthcare1558.92 -34.8 -2.18%

IDXCYCLIC…847.96 -0.67 -0.29%

IDX Techno.5397.17 -52.17 -0.96%

IDX Transp1882.68 -26.62 -1.39%

IDX Infrast….852.72 -12.36 -1.43%

IDX Finance1407.18 +2.27 +0.16%

IDX Banking1140.41 +5.97 +0.53#%

IDX Property….695 +7.00 +1.01%

Indo10Yr.6.8557 +0.0175 +0.26%

ICBI..349.7884 -0.4171 -0.12%

US5Yr 4.1712 -0.0390 -0.92%

US10Yr3.9220 -0.0270 -0.69%

US30Yr.3.9320-0.0060 -0.16%

VIX……. 20.95 -0.72 -3.32%

USDIndx104.6730-0.5410 -0.51%‼️

Como Indx.268.60 +1.45 +0.54%

(Core Commodity CRB)

BCOMIN….160.61 +2.63 +1.67%

IndoCDS..105.25 – -%

(5-yr INOCD5) (07/11)

IDR…..15270.00 +42.50 +0.28%‼️

Jisdor.15274.00 +58.00 +0.38%

Euro……1.0609 +0.0061 +0.58%

TLKM….25.94 -0.21 -0.80%

(3962)

EIDO……23.05 +0.17 +0.74%

EEM……38.50 +0.20 +0.52%

Oil…….75.68 -0.64 -0.84%

Gold 1824.90 +7.80 +0.43%

Timah 25651 – -%

(Closed 02/24)

Nickel.25398 +974.00 +3.99%‼️

(Closed 02/27)

Silver…….20.79 -0.14 -0.68%

Copper..401.10 +5.80 +1.47%

Nturl Gas.2.720 -0.006 -0.22%

Ammonia 4490.00 – -%

China

(Domestic Price)(02/23)

Coal price.196.50 -7.75 -3.79%‼️

(Mar/Newcastle)

Coal price.197.00 -6.00 -2.95%

(Apr/Newcastle)

Coal price.200.00 -5.80 -2.82%

(May/Newcastle)

Coal price.202.70 -6.35 -3.04%‼️

(Jun/Newcastle)

Coal price.148.15 -8.95 -5.70%‼️

(Mar/Rotterdam)

Coal price 148.10 -8.40 -5.37%‼️

(Apr/ Rotterdam)

Coal price148.15 -8.10 -5.18%‼️

(May/Rotterdam)

Coal price148.95 -7.75 -4.95%‼️

(Jun/Rotterdam)

CPO(May)….4228 +25 +0.59%

(Source: bursamalaysia.com)

Corn……..643.50 -5.75. -0.89%

SoybeanOil..60.34 -0.88 -1.44%

Wheat……710.00 -11.75 -1.63%

Wood pulp…5930.00 unch +0%

(Closed 02/27)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

US ijo, europe ijo, asia kemaren masih merah, sekarang harusnya nyusul ijo

oil gas coal turun, giliran metal2 naik, cuma silver yang merah. CPO ijo lagi. Kita cermati buy signal MDKA ANTM, dan kayanya AALI LSIP lanjut jalan lagi

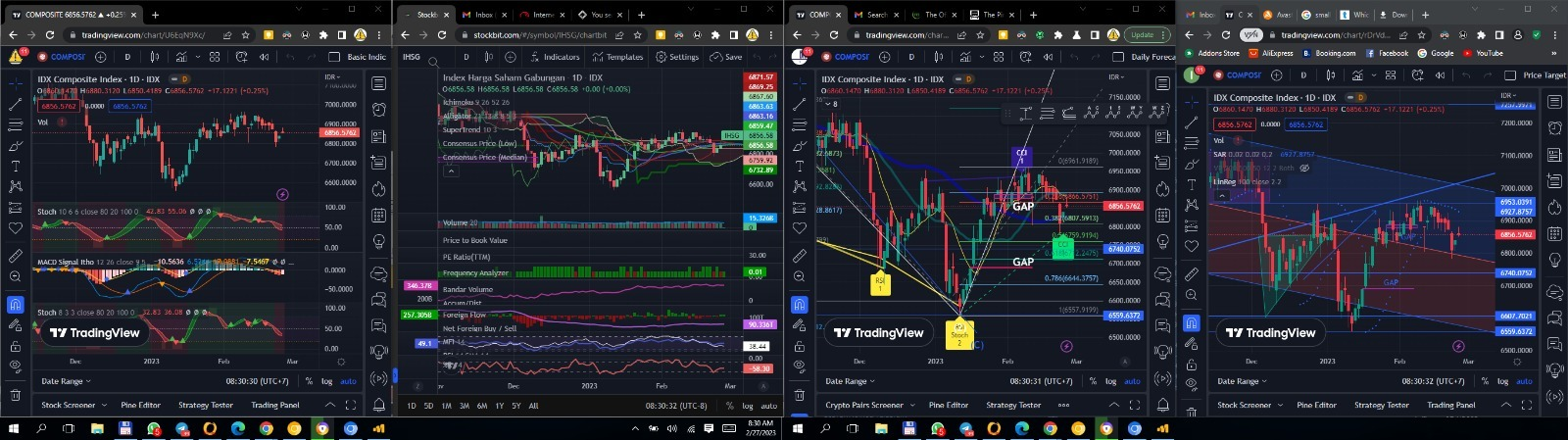

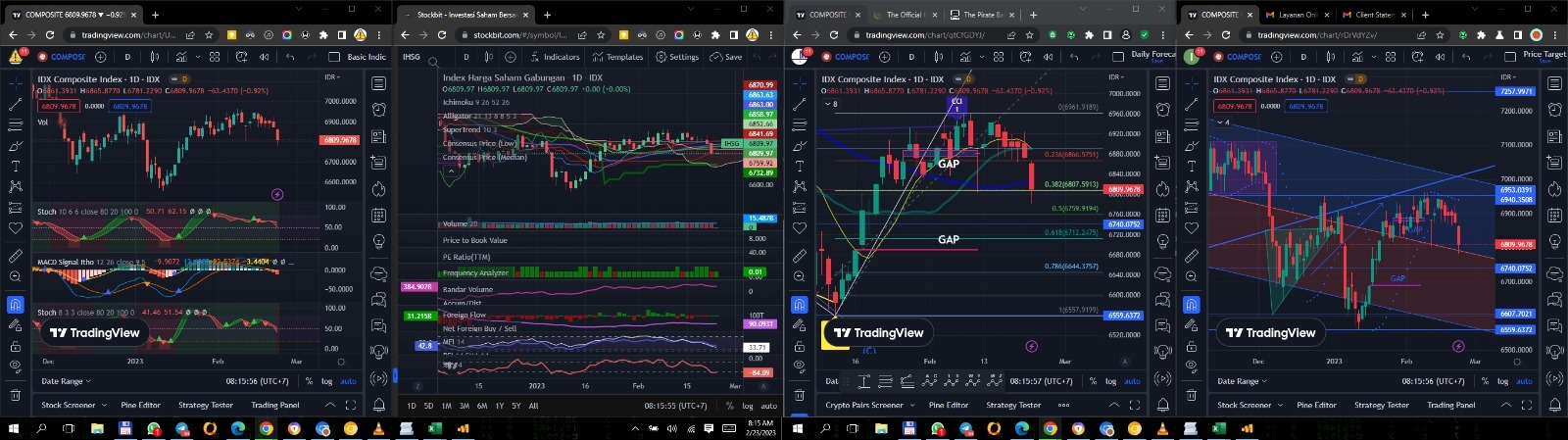

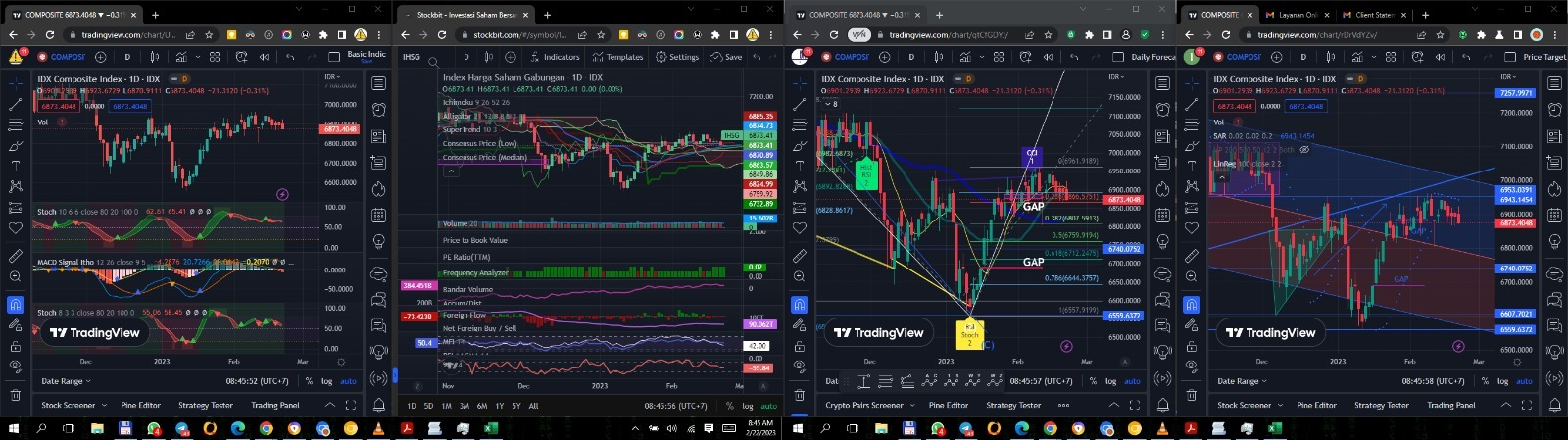

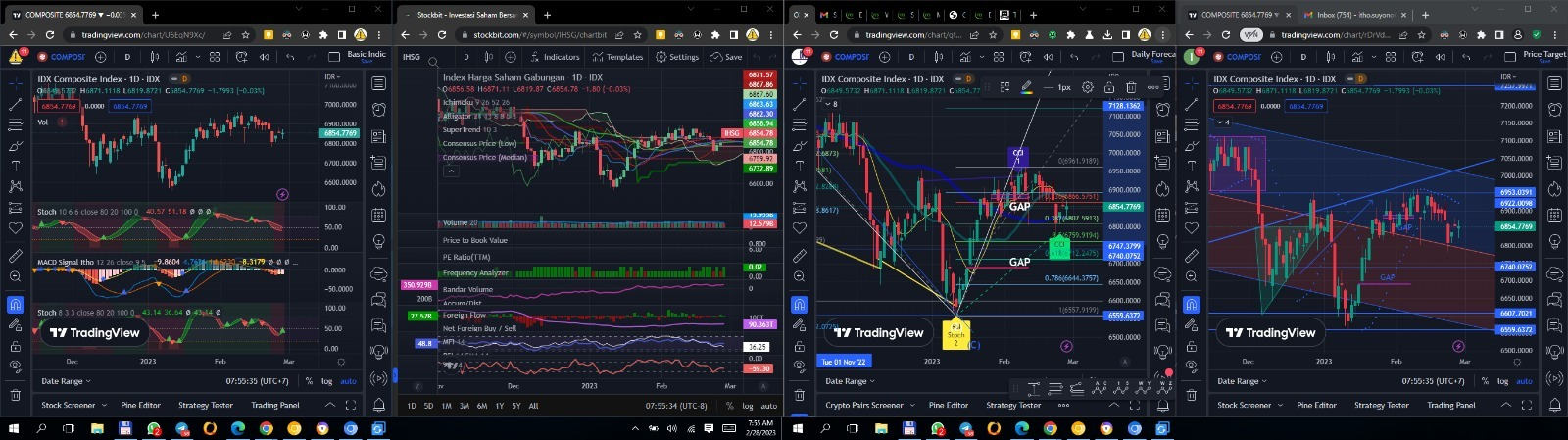

IHSG – kemaren udah tutup gap, US ijo semoga hari ini mulai lanjut rally. Stoch 833 udah buy, Masih NFS tipis, BD acc tipis, MFI masih down, mantul di midline LR

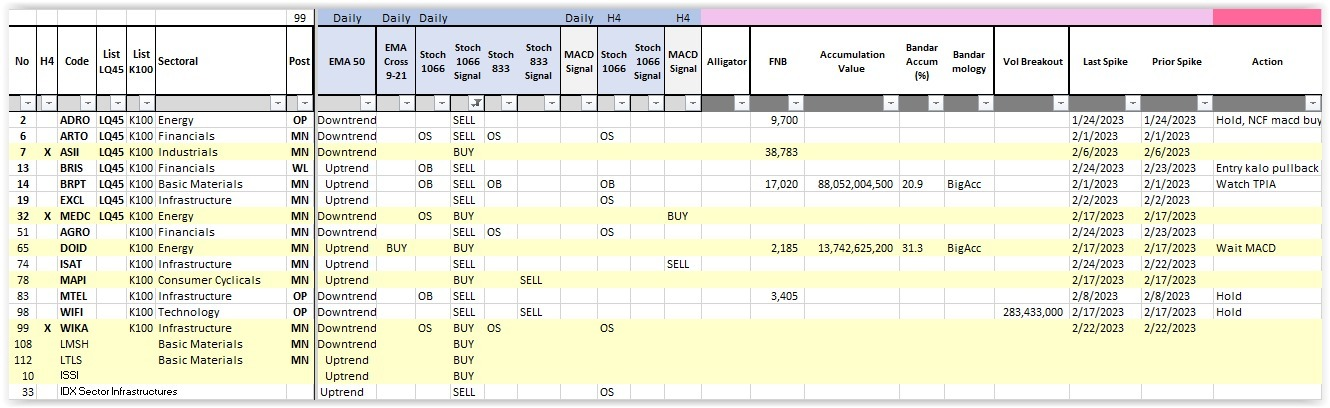

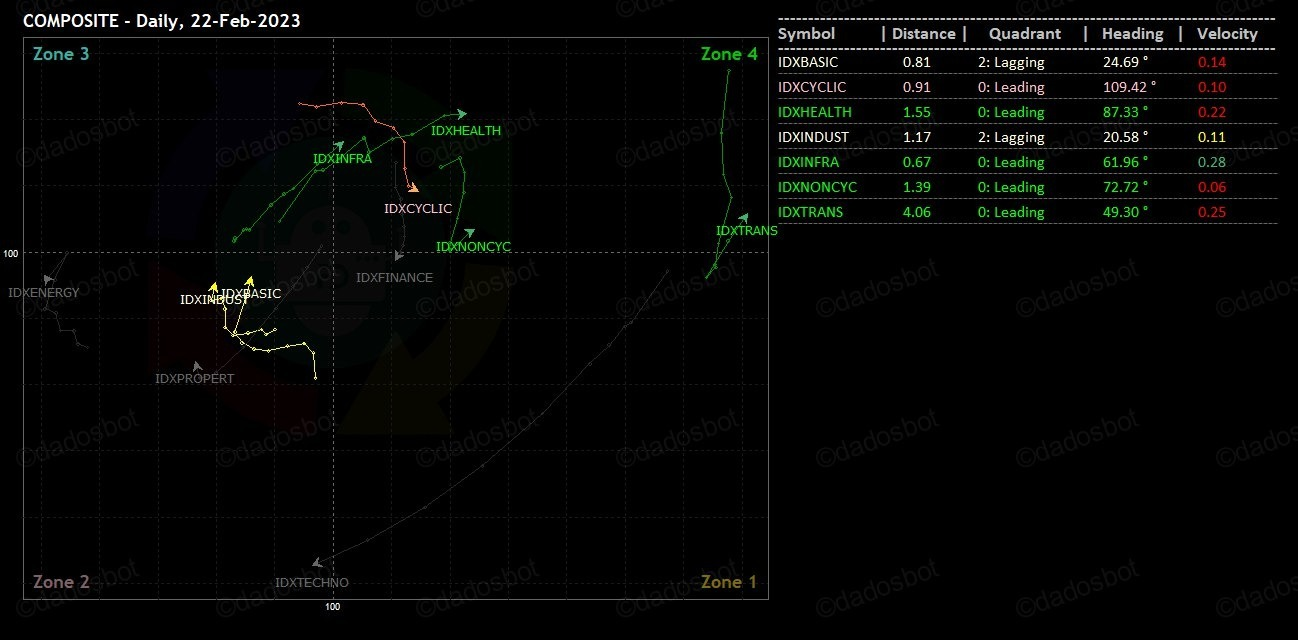

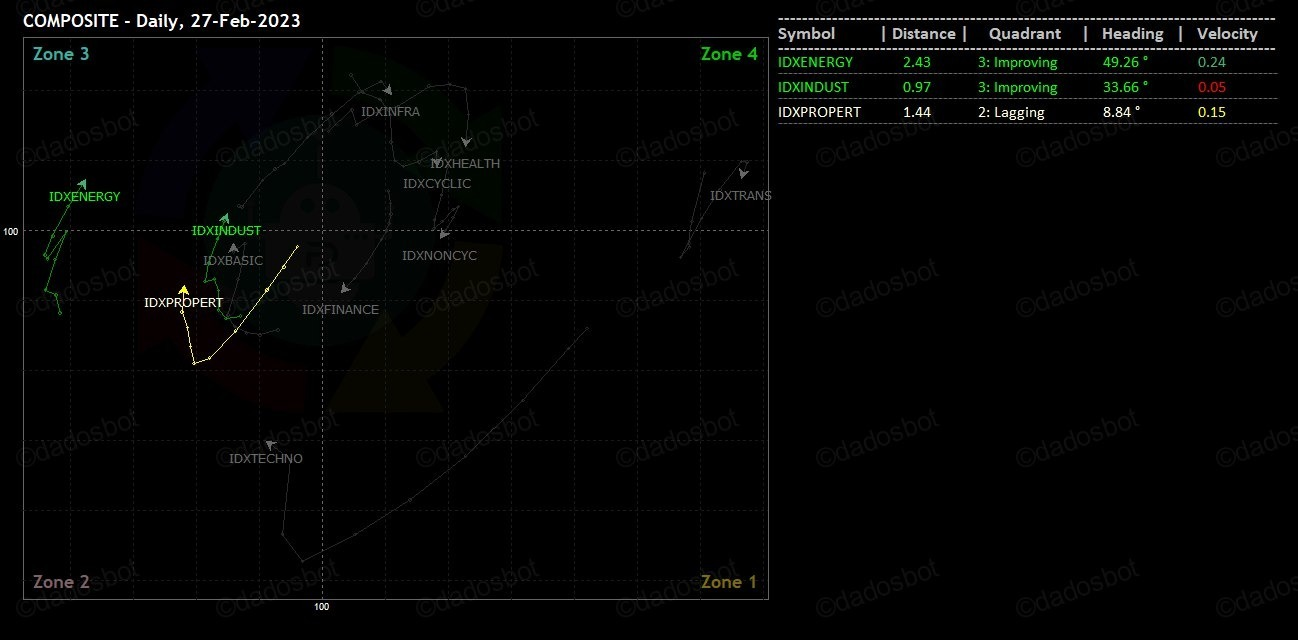

Leading sectors kemaren pada melemah, yang emerging Energy Industrials, Property sama Basic Materials

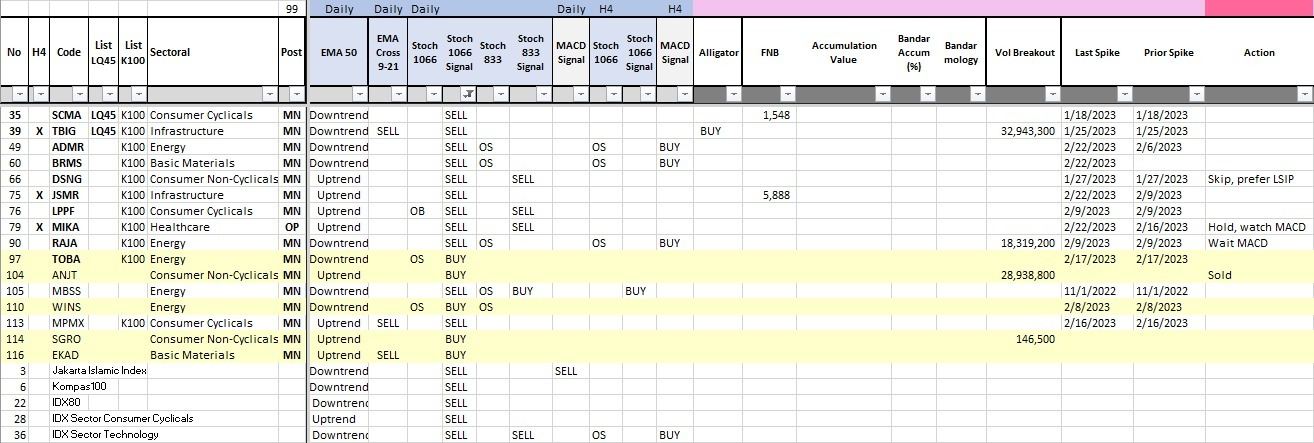

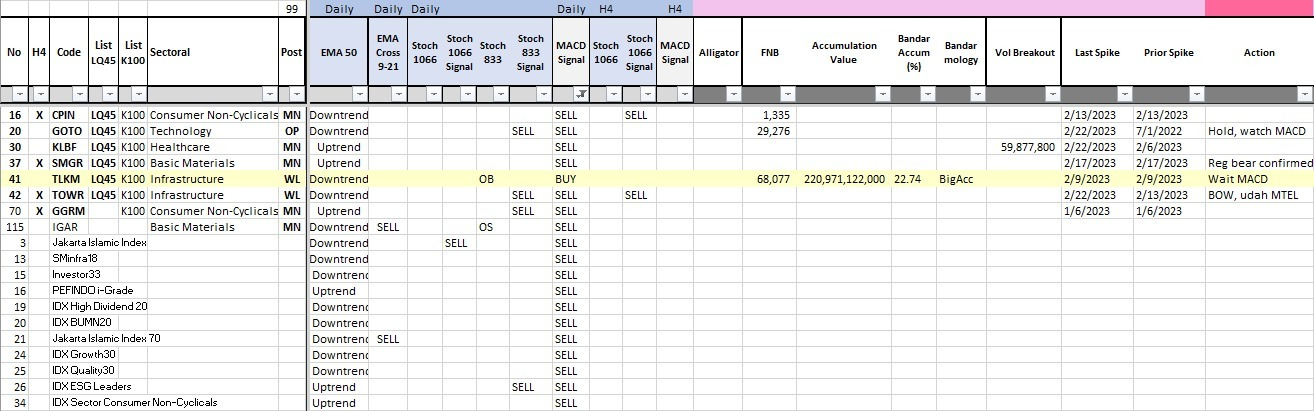

Stoch Buy Signal: TPIA UNTR UNVR PWON MBSS

MACD Buy SIgnal: ASII SRTG