Daily Analysis 20230810

August 10th, 2023

Good morning,

Dow sheds nearly 200 points, Nasdaq drops 1% as August slide resumes ahead of inflation report

Stocks fell Wednesday as Wall Street awaited fresh inflation data coming later in the week.

Dow……35123 -191.1 -0.54%

Nasdaq13722 -162.3 -1.17%

S&P 500.4468 -31.7 -0.70%

FTSE…..7587 +59.9 +0.80%

Dax……15853 +77.7 +0.49%

CAC……7322 +52.6 +0.72%

Nikkei…32204 -172.96 -0.53%

HSI…….19246 +61.9 +0.32%

Shanghai.3245 -16.1 -0.49%

IDX…..6875.11 +6.30 +0.09%

LQ45….965.30 +3.44 +0.36%

IDX30…501.17 +1.48 +0.30%

IDXEnergy…1912.13 -10.42 -0.54%

IDX BscMat.1098.62 -3.62 -0.33%

IDX Indstrl…1212.50 -0.29 -0.02%

IDXNONCYC.750.05 +4.32 +0.58%

IDX Hlthcare1488.99 -0.99 -0.07%

IDXCYCLIC….914.77 +2.86 +0.31%

IDX Techno.4453.84 -99.49 -2.18%

IDX Transp..1858.40 -28.97 -1.53%

IDX Infrast… .853.97 +3.61 +0.42%

IDX Finance.1430.66 -0.56 -0.04%

IDX Banking.1226.56+8.11 +0.67%

IDX Property..757 -8.90 -1.16%

Indo10Yr.6.3977+0.0035 +0.05%

ICBI….369.3157 +0.1254 +0.03%

US2Yr.4.8100 +0.050 +1.05%

US5Yr 4.1390 +0.025 +0.61%

US10Yr4.0100 -0.011 -0.27%

US30Yr.4.1650-0.027 -0.64%

VIX…….15.96 -0.03 -0.19%

USDIndx 102.4900 -0.0380 -0.04%

Como Indx…282.04 +2.82 +1.01%

(Core Commodity CRB)

BCOMIN….142.90 +0.05 +0.03%

IndoCDS.80.23 +2.03 +2.60%‼️

(5-yr INOCD5) (07/08)

IDR…..15189.50‼️-28.00 -0.18%

Jisdor.15206.00 ‼️-23.00 -0.15%

Euro……1.0977 +0.0022 +0.20%

TLKM…24.58 +0.35 +1.44%

(3738)

EIDO….23.07 +0.08 +0.35%

EEM…..40.09 +0.10 +0.25%

Oil…..84.23‼️ +1.53 +1.85%

Gold…1948.90‼️ -10.50 -0.54%

Timah..27300.00 -456.00 -1.64%

(Closed 08/08)

Nickel..20518.50 -358.50 -1.72%

(Closed 09/08)

Silver…… 22.74 -0.09 -0.39%

Copper.378.60 +1.10 +0.29%

Iron Ore 62% 104.41 -0.32 -0.31%

(08/08)

Nturl Gas.2.7920 +0.1700 +6.09%‼️

Ammonia China..3366.67 -16.6 -0.49%

(Domestic Price)(08/08)

Coal price..142.50 unch +0%

(Agt/Newcastle)

Coal price.148.25 +3.00 +2.07%

(Sept/Newcastle)

Coal price.150.90 +2.65 +1.79%

(Oct/Newcastle)

Coal price.154.25 +2.35 +1.55%

(Nov/Newcastle)

Coal price115.85 +1.10 +0.96%

(Agt/Rotterdam)

Coal price.120.60 +2.60 +2.20%

(Sept/ Rotterdam)

Coal price.120.65 +1.65 +1.39%

(Oct/Rotterdam)

Coal price.122.40 +1.60 +1.32%

(Nov/Rotterdam)

CPO(Oct)..3765 +73 +1.97%

(Source: bursamalaysia.com)

Corn………494.25 -4.50 -0.90%

SoybeanOil 60.43 +0.58 +0.97%

Wheat…..661.75 -4.50 -2.90%

Wood pulp..4600.00‼️ +40 +0.88%

(Closed 09/08)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

US closing merah, Europe ijo, Asia Varied, ID Sing Korea Hongkong ijo, Jepang China merah

USD index turun tipis, ga terlalu ngaruh, Gold Silver iron ore merah, copper ijo tipis, timah nikel lanjut merah, Oil Gas lanjut ijo, Coal ijo, CPO lijo. Masih sideways buat ANTM MDKA, hati2 TINS INCO NCKL

IHSG – indicator type oscillators masih bilang belum ok, tapi rada pede karena FNB. Diharapkan galama konsolidasi terus breakout ke atas, Big Banks udah mulai jalan, kemaren keganjel GOTO yang dibanting juga tetep berhasil closing ijo, semoga lanjut, walau sepertinya masih sideways dulu

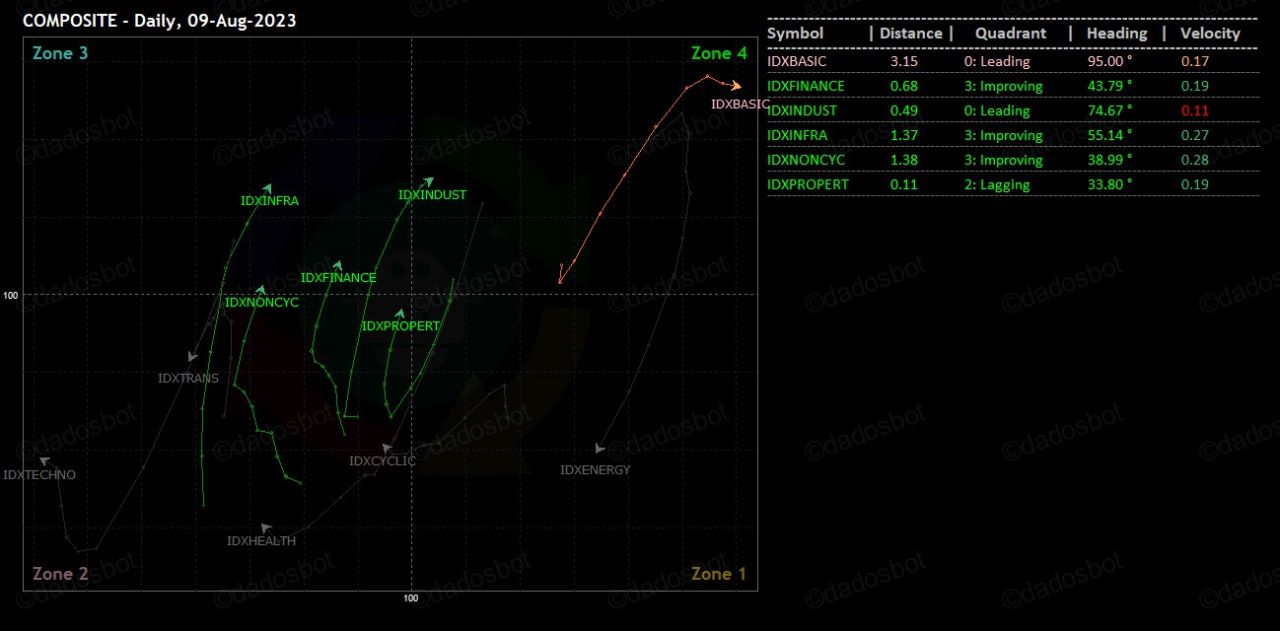

Basic Materials, Industrials, Property, Financials, Infrastructure, Consumer Non-Cyclicals

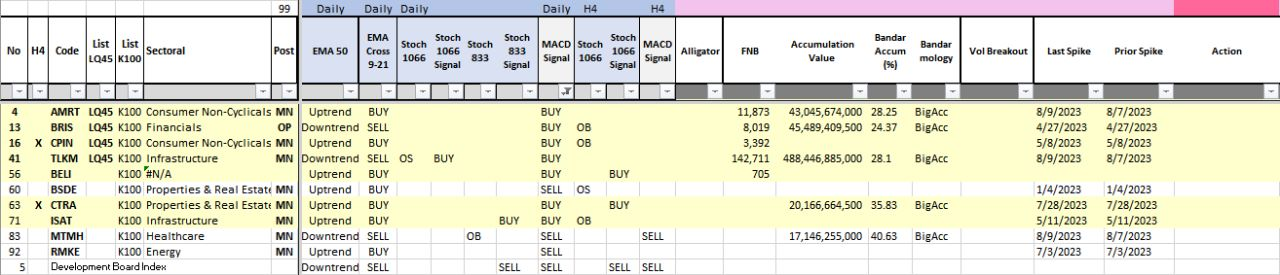

Stochastic Buy Signal: BMRI PTBA TLKM AALI BDMN BSSR JPFA TINS RDTX INDS

MACD Buy Signal: AMRT BRIS CPIN TLKM BELI CTRA ISAT

Alligator Buy Signal: ADMR MTEL

Supertrend Buy Signal: JPFA