January 04th, 2024

Good morning,

Dow tumbles nearly 300 points Wednesday, Nasdaq closes lower for a 2nd straight day in 2024

The Nasdaq Composite

fell for a second session Wednesday to start the year, building on its worst daily performance in nearly three months.

Dow……37430 -284.9 -0.76%

Nasdaq14592 -173.7 -1.18%

S&P 500.4705 -38.02 -0.80%

FTSE…..7682 -39.2 -0.51%

Dax……16538 -230.97 -1.38%

CAC……7412 -119.0 -1.58%

Nikkei..33464 closed +0%

HSI…….16646 -142.1 -0.85%

Shanghai.2967 +4.97 +0.17%

IDX…..7379.09 -44.50 -0.61%

LQ45….973.38 -6.05 -0.38%

IDX30…494.25 -4.17 -0.84%

IDXEnergy..2134.80 -8.16 -0.38%

IDX BscMat.1326.31 -5.83 -0.44%

IDX Indstrl…1103.81 -1.70 -0.15%

IDXNONCYC.718.44 -5.97 -0.82%

IDX Hlthcare1341.16 -12.40 -0.92%

IDXCYCLIC…825.24 +3.63 +0.44%

IDX Techno4418.00 +0.19 +0.02%

IDX Transp 1656.97 +2.01 +0.12%

IDX Infrast 1577.29. +0.98 +0.06%

IDX Finance.1448.02 -4.07. -0.28%

IDX Banking.1267.99 -1.01 -0.08%

IDX Property.. 709 -0.90 -0.12%

Indo10Yr.6.6494+0.0333 +0.50%

ICBI…374.1959 -0.4937 -0.13%

US2Yr.4.333 +0.009 +0.21%

US5Yr 3.905 -0.017 -0.43%

US10Yr3.920 -0.021 -0.53%

US30Yr.4.070-0.013 -0.32%

VIX….14.04 +0.84 +6.36%‼️

USDIndx 102.4570 +0.221 +0.22%

Como Indx..265.25 +2.62 +1.00%

BCOMIN……139.93 -1.24 -0.88%

IndoCDS..69.23 -0.06 -0.09%

(5-yr INOCD5) (02/01)

IDR…..15481.00 +11.00 +0.07%

Jisdor.15495.00 +22.00 +0.14%

Euro….1.0920 -0.0022 -0.20%

TLKM…25.62 -0.28 -1.08%

(3970)

EIDO….22.05 -0.16 -0.72%

EEM….39.52 -0.22 -0.55%

Oil……..72.70 +2.32 +3.30%‼️

Gold..2042.80 -30.60 -1.48%

Timah..25184.00 -231 -0.91%

(Closed 02/01)

Nickel..16425.00 -140 -0.85%

(Closed 03/01)

Silver……23.16 -0.80 -3.32%

Copper.386.15 -1.90 -0.49%

Iron Ore 62% 136.37 – -%

(02/01)

Nturl Gas..2.687 +0.113 +4.39%‼️

Ammonia China.3656.67 +33.34 +0.92%

(Domestic Price)(02/02)

Coal price.128.50 +0.75 +0.59%

(Jan/Newcastle)

Coal price 127.09 +0.15 +0.67%

(Feb/Newcastle)

Coal price.125.75 +0.90 +0.72%

(Mar/Newcastle)

Coal price 124.40 +0.50 +0.40%

(Apr/Newcastle)

Coal price.108.95 +2.80 +2.64%

(Jan/Rotterdam)

Coal price 103.75 +2.20 +2.17%

(Feb/Rotterdam).

Coal price. 99.25 +2.15 +2.21%

(Mar/Rotterdam)

Coal price .97.20 +2.00 +2.10%

(Apr/Rotterdam)

CPO(Mar)..3624 -36 -0.98%

(Source: bursamalaysia.com)

Corn……465.25 +1.50 +0.32%

SoybeanOil 48.60 +0.31 +0.64%

Wheat….600.25 -6.50 -1.07%

Wood pulp..5050.00 +10 +0.20%

(Closed 02/01)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

Update Global Economic Calendar

3 Jan 2023

GERMANY MARKET :

Unemployment Change (Dec)

Actual : 5K

Forecast : 20K

Previous : 22K

Unemployment Rate (Dec)

Actual : 5.9%

Forecast : 5.9%

Previous : 5.9%

Unemployment Persons (Dec)

Actual : 2.703M

Forecast : –

Previous : 2.702M

U.S MARKET :

MBA Mortgage Applications (Dec/29)

Actual : -10.7%

Forecast : –

Previous : -1.5%

MBA 30-Year Mortgage Rate (Dec/29)

Actual : 6.76%

Forecast : –

Previous : 6.83%

ISM Manufacturing PMI (Dec)

Actual : 47.4

Forecast : 47.1

Previous : 46.7

ISM Manufacturing Employment (Dec)

Actual : 48.1

Forecast : 46.1

Previous : 45.8

ISM Manufacturing New Orders (Dec)

Actual : 47.1

Forecast : –

Previous : 48.3

By PHINTRACO SEKURITAS | Research

– Disclaimer On –

US merah dalem, keliatanya karena release berita ISM manufacturing unemployment dan new order turun. europe merah, asia juga, IHSG kemaren memang sudah diduga jadwal turun, sekarang diharap naik tapi kalo global merah semua rada berat. Semoga hanya sideways atau koreksi kecil

US bond rates ga banyak rubah, USD index naik, metal turun semua, oil gas coal naik, CPO masih turun. Kayanya belum jalan ini ANTM INCO TINS MDKA, tapi harusnya major udah uptrend. AALI LSIP juga

IHSG – stoch up flattening OB, MACD up flattening, MFI sw, w% masih uptrend, BD mulai dist, FNS, udah di wave 5, agak mengkhawatirkan…

Cacing RSI malah all good, Consumer Non-Cyclicals sama Consumer Cyclicals yang arahnya paling bagus

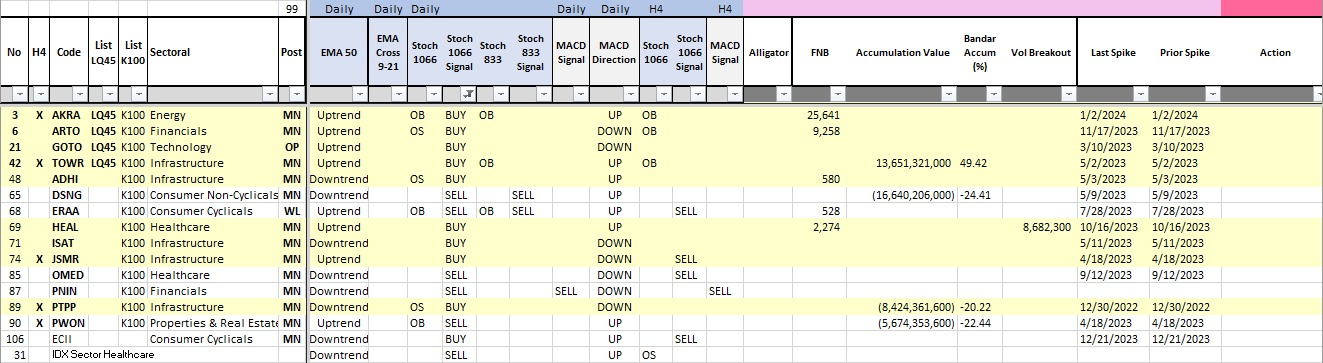

Stochastic Buy Signal: AKRA ARTO GOTO TOWR ADHI HEAL ISAT JSMR PTPP. yang big accum cuma TOWR

MACD Buy Signal: BRIS BBKP BRMS Big accum BRIS BBKP

Stochastic Continuation Signal: INCO big acc MPMX spike