Daily Analysis 20230502

May 02nd 2023

Good morning,

Dow closes slightly lower following JPMorgan’s takeover of fallen First Republic

The Dow Jones Industrial Averag

e inched lower Monday in the wake of the government’s seizure of First Republic over the weekend and the bank’s subsequent sale to JPMorgan Chase.

Dow……34052 -46.5 -0.14%

Nasdaq12213 -13.99 -0.11%

S&P 500.4168 -1.6 -0.04%

FTSE…..7871 closed +0%

Dax……15922 closed +0%

CAC……7492 closed +0%

Nikkei…..29123 +266.7 +0.92%

HSI………19895 closed +0%

Shanghai.3323 closed +0%

IDX…..6915.72 closed +0%

LQ45….961.75 closed +0%

IDX30…501.01 closed +0%

IDXEnergy…2094.86 closed +0%

IDX BscMat 1171.17 closed +0%

IDX Indstrl…1207.23 closed +0%

IDXNONCYC.726.67 closed +0%

IDX Hlthcare1541.67closed +0%

IDXCYCLIC…..810.83closed +0%

IDX Techno..4937.07’closed +0%

IDX Transp..1809.88 closed +0%

IDX Infrast…..822.05 closed +0%

IDX Finance.1385.54 closed +0%

IDX Banking.1151.04 closed +0%

IDX Property…700 closed +0%

Indo10Yr.6.7151 closed +0%

ICBI….356.7992 closed +0%

US2Yr.4.1407 +0.1199 +2.98%

US5Yr 3.6328 +0.1345 +3.84%‼

US10Yr3.5700+0.1370 +3.84%‼

US30Yr.3.8090+0.1270 +3.45%‼

VIX…… 16.08 +0.30 +1.90%

USDIndx102.1510 +0.6480 +0.64%

Como Indx.266.32 -1.83 -0.68%

(Core Commodity CRB)

BCOMIN…154.49 +0.59 +0.38%

IndoCDS..90.11 -8.90 -8.98%👍

(5-yr INOCD5) (28/04)

IDR…..14674.50👍 closed +0%

Jisdor.14661.00👍 closed +0%

Euro……1.0975 -0.0044 -0.40%

TLKM..28.51 -0.29 -1.01%

(4180)

EIDO….24.68 -0.07 -0.26%

EEM….39.00 -0.13 -0.33%

Oil……75.68 -1.10 -1.43%

Gold.1991.20 -7.90 -0.40%

Timah..26088.00 closed +0%

(Closed 28/04)

Nickel..24259.00 closed +0%

(Closed 28/04)

Silver……25.25 +0.02 +0.08%

Copper…393.40 +4.35 +1.12%

Nturl Gas.2.313 -0.0850 -3.54%

Coal price.185.15 closed +0%

(May/Newcastle)

Coal price.187.60 closed +0%

(Jun/Newcastle)

Coal price.191.60 closed +0%

(Jul/Newcastle)

Coal price.195.85 closed +0%

(Agt/Newcastle)

Coal price.136.40 closed +0%

(May/Rotterdam)

Coal price.132.80 closed +0%

(Jun/ Rotterdam)

Coal price 131.80 closed +0%

(Jul/Rotterdam)

Coal price 136.40 closed +0%

(Agt/Rotterdam)

CPO(Jul)…3353 closed +0%

(Source: bursamalaysia.com)

Corn……..584.50 -0.50 -0.09%

SoybeanOil51.81 +0.14 +0.17%

Wheat….618.25 -15.50 -2.45%

Wood pulp..4000.00 unch +0%

(Closed 01/05)

©Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

US closing merah kemaren, Europe closed, Asia kebanyakan tutup, Nikkei ijo. Interest Rate US naik lagi, ga bagus buat saham ini

Oil gas merah, coal market (Newcastle/Rotterdam) closed, Gold merah, silver copper ijo

IHSG – Stoch Up, MACD up, MFI flat, w% masih uptrend, BD FF acc, rejection candle di fibo 50, tapi harusnya masih firm retracement pattern, sekalian breakout double bottom. Semoga cepet rally lagi

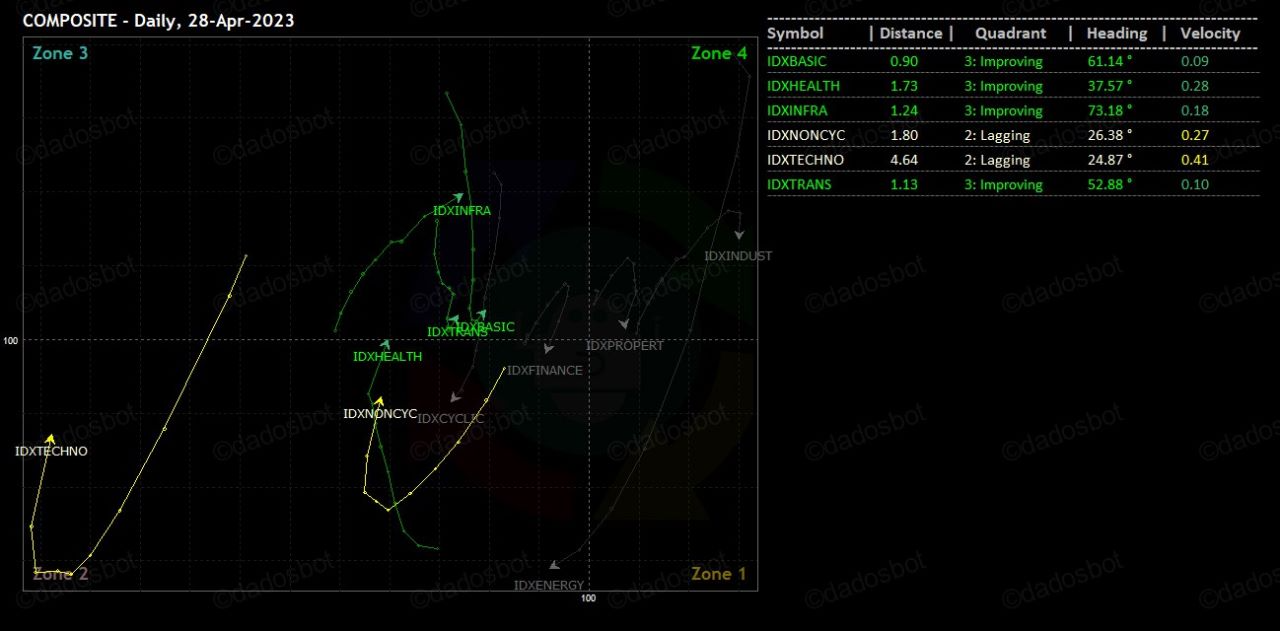

Industrials melemah, Infrastructure, Basic Materials, Transportation siap jalan, Technology Healthcare sama Consumer Non-Cyclicals terlihat mau nyusul. Financials melemah, kalo lanjut melemah bahaya buat index

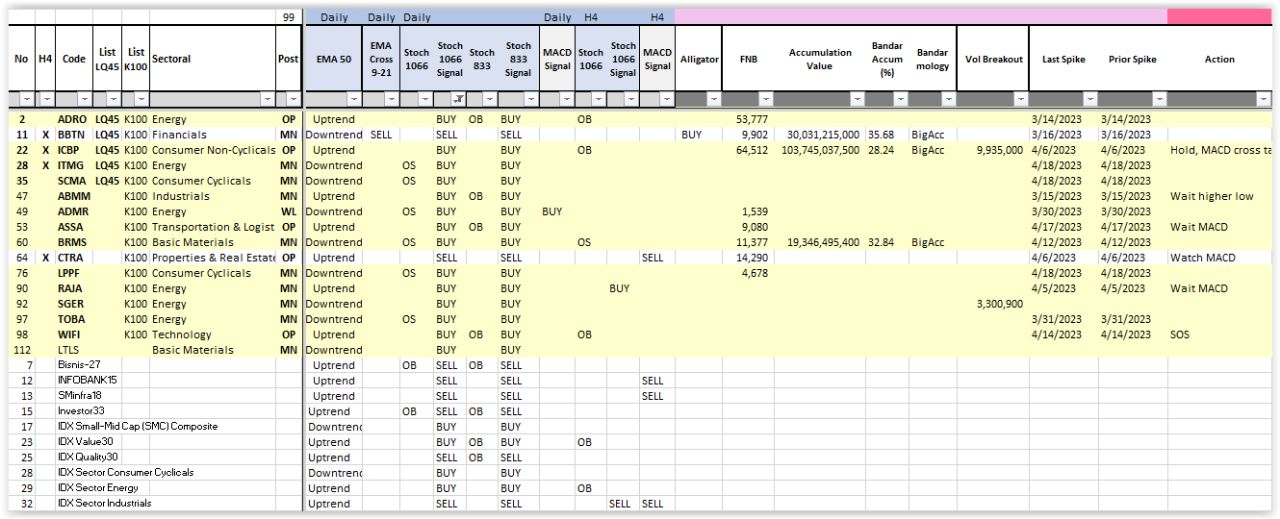

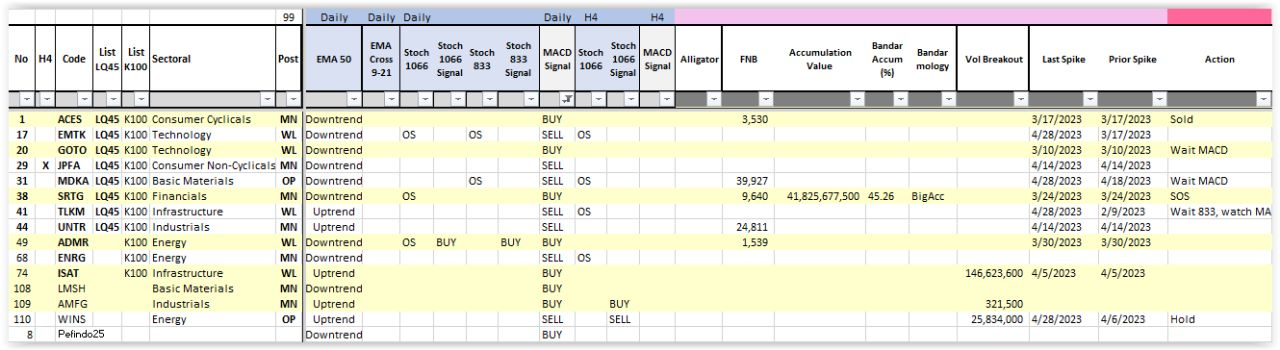

Stochastic Buy Signal banyak, kita sort yang FNB atau BD accum: ADRO ICBP ADMR ASSA BRMS LPPF

MACD Buy Signal: ACES GOTO SRTG ADMR ISAT

Alligator Buy Signal: BBTN TOWR