Daily Analysis 20230524

May 24th, 2023

Good morning,

The three major averages fell during regular trading Tuesday.

Treasury Secretary Janet Yellen previously warned lawmakers that a potential default in early June is “highly likely.” House Speaker Kevin McCarthy said he had a “productive” discussion with President Joe Biden on Monday. Nonetheless, there were few indicators of progress made in negotiations on Tuesday.

Dow……33056 -231.1 -0.69%

Nasdaq12560 -160.5 -1.26%

S&P 500.4146 -47.1 -1.12%

FTSE…..7763 -8.04 -0.10%

Dax……16153 -71.1 -0.44%

CAC……7379 -99.5 -1.33%

Nikkei…..30958 -129.1 -0.42%

HSI………19431 -246.9 -1.25%

Shanghai.3246 -50.2 -1.52%

IDX…..6736.68 +7.04 +0.10%

LQ45….946.11 +0.68 +0.07%

IDX30…492.56 +0.41 +0.08%

IDXEnergy…1813.88 -14.91 -0.82%

IDX BscMat 1024.79 -6.78 -0.66%

IDX Indstrl…1178.34 +4.57 +0.39%

IDXNONCYC.742.15 +1.66 +0.22%

IDX Hlthcare1502.10 +2.42 +0.16%

IDXCYCLIC…861.11 +11.60 +1.37%.

IDX Techno..4756.94 -46.11 -0.96%

IDX Transp..1832.06 +25.91 +1.43%

IDX Infrast…..811.97 -4.11 -0.50%

IDX Finance.1385.16 +2.57 +0.19%

IDX Banking.1160.77 +4.27 +0.37%

IDX Property…..725 +0.40 +0.06%

Indo10Yr.6.5470 +0.0041 +0.06%

*ICBI..361.3690* +0.1375 +0.04%

*US2Yr.4.3230* +0.0033 +0.08%

*US5Yr 3.7426* +0.0037 +0.10%

*US10Yr3.6980* -0.019 -0.51%

*US30Yr.3.9580*-0.0090 -0.24%

*VIX……18.53 +1.32 +7.67%‼️*

*USDIndx103.4880‼️+0.29 +0.28%*

Como Indx.261.21 -0.37 -0.14%

(Core Commodity CRB)

BCOMIN…141.97 -2.16 -1.50%

*IndoCDS.91.62 -4.30 -4.48%👍*

(5-yr INOCD5) *(22/05)*

*IDR…..14875.00‼️ -15.00 -0.10%*

*Jisdor.14878.00‼️ -19.00 -0.13%*

*Euro……1.0773‼️ -0.0041 -0.38%*

TLKM..27.02 -0.09 -0.33%

*(4020)*

EIDO….23.79 -0.07 -0.29%

EEM…..38.69 -0.61 -1.55%

*Oil…..73.69 +1.70 +2.36%*

*Gold…1996.00* +3.90 +0.20%

*Timah..24950.00 -501.00 -1.97%*

*(Closed 22/05)*

*Nickel..20970.50 -392.00 -1.83%*

(Closed 23/05)

Silver……23.79 -0.19 -0.80%

Copper…364.30 -3.50 -0.95%

Iron Ore 62% 107.17 +0.06 +0.06%

(22/05)

Nturl Gas.2.509 -0.038 -1.49%

Coal price.160.00 -0.35 -0.22%

(May/Newcastle)

Coal price.161.25 -2.15 -1.32%

(Jun/Newcastle)

Coal price.158.10 -2.65 -1.65%

(Jul/Newcastle)

Coal price.159.80 -2.85 -1.75%

(Agt/Newcastle)

Coal price.119.00 unch +0%

(May/Rotterdam)

*Coal price.105.20 -2.55 -2.37%*

(Jun/ Rotterdam)

*Coal price.100.70 -2.55 -2.47%*

(Jul/Rotterdam)

*Coal price…99.85 -2.85 -2.77%*

(Agt/Rotterdam)

CPO(Agt)…3381 -48.00 -1.40%

(Source: bursamalaysia.com)

Corn……577.00 +6.50 +1.14%

*SoybeanOil 47.76 -1.01 -2.07%*

*Wheat……622.25 +16.00 +2.64%*

Wood pulp..4100.00 +20 +0.49%

(Closed 23/05)

©️Phintraco Sekuritas

Broker Code: *_AT_*

_Desy Erawati/ *DE*_

*Source*: Bloomberg, Investing, IBPA, CNBC, Bursa Malaysia

_Copyright: Phintraco Sekuritas_

Prepare merah hari ini, US Europe asia merah kemaren, IDX sempet tinggi closing ijo tipis

Oil ijo, gas coal merah, gold iron ore ijo, metal lain merah, CPO lanjut merah

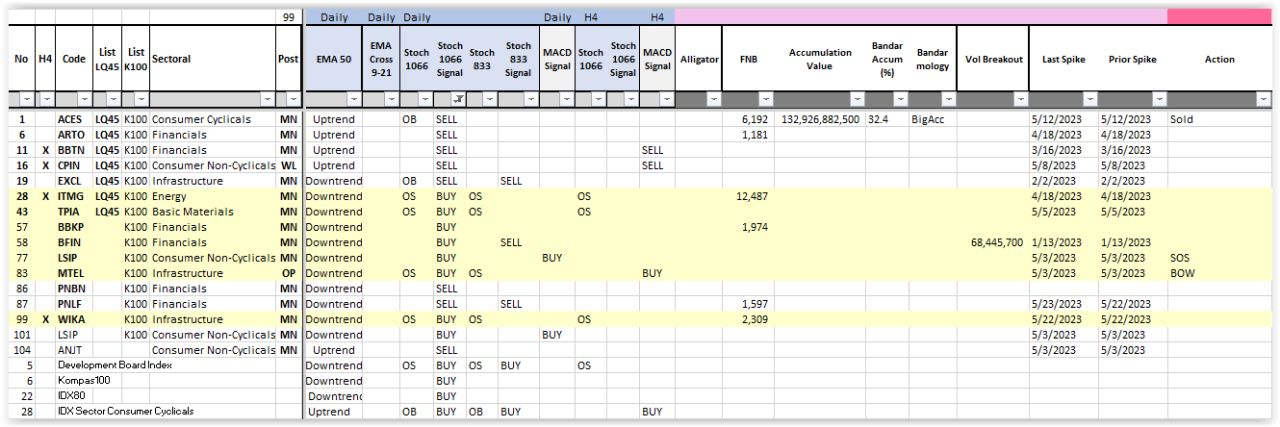

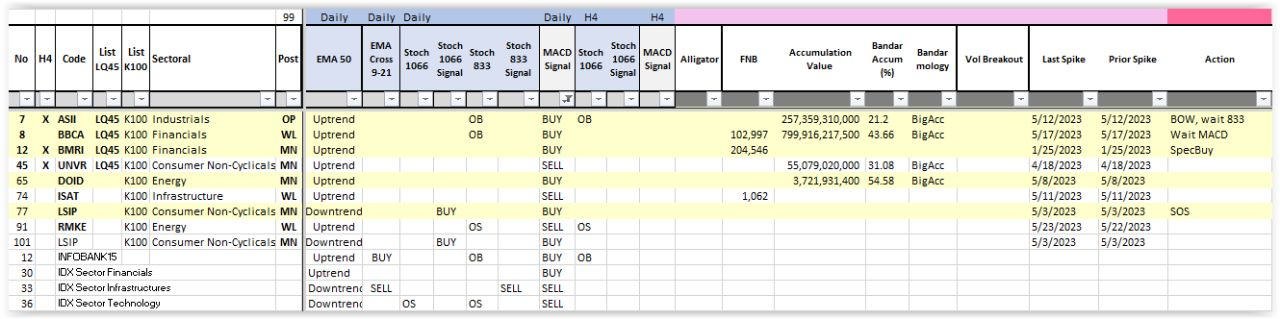

IHSG – 3 white soldiers, walau candle terakhir long upper shadow, sign of reversal, tapi hari ini kemungkinan merah dulu. Stoch buy, macd rev up, MFIup, w% up, BD sw, FF acc, retracement pattern in motion, harusnya towards fibo 61

Healthcare Industrials, Financials nya melemah

Stochastic Buy Signal: ITMG TPIA BBKP BFIN LSIP MTEL

MACD Buy Signal: ASII BBCA BMRI DOID LSIP