What Is the Asian Infrastructure Investment Bank (AIIB)?

The Asian Infrastructure Investment Bank (AIIB) is a new international development bank that provides financing for infrastructure projects in Asia. It began operations in January 2016.

How the Asian Infrastructure Investment Bank (AIIB) Works

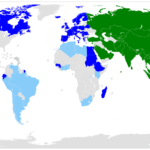

The Asian Infrastructure Investment Bank (AIIB) is a multilateral development bank headquartered in Beijing. Like other development banks, its mission is to improve social and economic outcomes in its region, Asia, and beyond. The bank opened in January 2016 and now has 105 approved members worldwide, as of Jul. 30, 2022.

The History of the Asian Infrastructure Investment Bank

China’s leader Xi Jinping first proposed an Asian infrastructure bank at an APEC summit in Bali in 2013. Many observers have interpreted the bank as a challenge to international lending bodies, which some consider too reflective of American foreign policy interests such as the International Monetary Fund (IMF), the World Bank and the Asian Development Bank.

In this bank’s case, China controls half of the bank’s voting shares, which gives the perception that the AIIB will function in the interests of the Chinese government. The U.S. has questioned the bank’s governing standards and its social and environmental safeguards, perhaps pressuring allies not to apply for membership. However, despite American objections, approximately half of NATO has signed on, as has nearly every large Asian country, with the exception of Japan. The result is widely considered in an indicator of China’s growing international influence at the expense of the United States.

The Structure of the Asian Infrastructure Investment Bank

The bank is headed by a Board of Governors composed of one Governor and one Alternate Governor appointed by each of the 86 member countries. A non-resident Board of Directors is responsible for the direction and management of the Bank such as the Bank’s strategy, annual plan and budget and establishing policies and oversight procedures.

The bank staff is headed by a President who is elected by AIIB shareholders for a five-year term and is eligible for re-election once. The President is supported by Senior Management including five Vice Presidents for policy and strategy, investment operations, finance, administration, and the corporate secretariat and the General Counsel and Chief Risk Officer. Mr. Jin Liqun is the current President.

Asian Infrastructure Investment Bank Priorities

The bank’s priorities are projects that promote sustainable Infrastructure and to support countries that are striving to meet environmental and development goals. The bank funds projects linking countries in the region and cross-border infrastructure projects for roads, rail, ports, energy pipelines and telecoms across Central Asia and maritime routes in South East and South Asia and the Middle East. The bank’s priorities also include private capital mobilization and encouraging partnerships that stimulate private capital investment such as those with other multilateral development banks, governments, and private financiers.

An example of an AIIB project is a rural road connectivity initiative that will benefit approximately 1.5 million rural residents in Madhya Pradesh, India. In April 2018, the AIIB announced the project, which is also expected to improve the livelihoods, education, and mobility of the residents of 5,640 villages. The project is a U.S. $140-million jointly financed by the AIIB and the World Bank.

The 2011 U.S. Debt Ceiling Crisis was a contentious debate in Congress that occurred in July 2011 regarding the maximum amount of debt the federal government should be allowed.

Key Takeaways

The 2011 U.S. Debt Ceiling Crisis was one of a series of recurrent debates over increasing the total size of the U.S. national debt.

In 2008, the federal budget deficit stood at $458.6 billon, which widened to $1.4 trillion the following year as the government spent heavily to boost the economy.

To resolve the crisis, Congress passed a law that increased the debt ceiling by $2.4 trillion.

Understanding the 2011 U.S. Debt Ceiling Crisis

The federal government has rarely achieved a balanced budget, and its budget deficit ballooned following the 2007-08 Financial Crisis. In the 2008 fiscal year, the deficit stood at $458.6 billon, widening to $1.4 trillion in 2009 as the government engaged in a massive fiscal policy response to the economic downturn.

Between 2008 and 2010, Congress raised the debt ceiling from $10.6 trillion to $14.3 trillion. In 2011, as the economy showed early signs of recovery and federal debt approached its limit once again, negotiations began in Congress to balance spending priorities against the ever-rising debt burden.

Heated debate ensued, pitting proponents of spending and debt against fiscal conservatives. Pro-debt politicians argued that failing to raise the limit would require immediate cuts to spending already authorized by Congress, which could result in late, partial, or missed payments to Social Security and Medicare recipients, government employees, and government contractors.

Moreover, they asserted the Treasury could suspend interest payments on existing debt rather than withhold funds committed to federal programs. The prospect of cutting back on already promised spending was labeled a crisis by debt proponents.

On the other hand, the specter of a technical default on existing Treasury debt roiled financial markets. Fiscal conservatives argued that any debt limit increase should come with constraints on the growth of federal spending and debt accumulation.

Outcome of the 2011 U.S. Debt Ceiling Crisis

Congress resolved the debt ceiling crisis by passing the Budget Control Act of 2011, which became law on August 2, 2011. This act allowed the debt ceiling to be raised by $2.4 trillion in two phases, or installments.

In the first phase, a $400 billion increase would occur immediately, followed by another $500 billion unless Congress disapproved it. The second phase allowed for an increase between $1.2 trillion and $1.5 trillion, subject to Congressional disapproval as well. In return, the act included $900 billion in slowdowns in planned spending increases over a 10-year period. It also established a special committee charged with finding at least $1.5 trillion in additional savings.

In effect, the legislation incrementally raised the debt ceiling from $14.3 trillion to $16.4 trillion by January 27, 2012.

Following the passage of the act, Standard & Poor’s took the radical step of downgrading the United States long-term credit rating from AAA to AA+, even though the U.S. did not default. The report says, “The downgrade reflects our opinion that the fiscal consolidation plan that Congress and the Administration recently agreed to falls short of what, in our view, would be necessary to stabilize the government’s medium-term debt dynamics.” The credit rating agency cited the unimpressive size of deficit reduction plans relative to the likely future prospects for politically driven spending and debt accumulation.

Debt Approval Process Leading to the 2011 U.S. Debt Ceiling Crisis

The U.S. Constitution gives Congress the power to borrow money. Before 1917, this power was exercised by Congress authorizing the Treasury to borrow specified amounts of debt to fund limited expenses, such as war-time military spending, which would be repaid after the end of hostilities. This kept the national debt directly linked to authorized spending.

In 1917, Congress imposed a limit on federal debt as well as individual issuance limits. In 1939, Congress gave the Treasury more flexibility in how it managed the overall structure of federal debt, giving it an aggregate limit. However, by delegating debt management authority to the Treasury, Congress was able to break the direct connection between authorized spending and the debt that finances it.

While allowing greater flexibility to raise spending, this practice also created a need for Congress to repeatedly raise the debt limit when spending threatens to overrun available credit. Due to occasional political resistance to the idea of continually expanding the federal debt, this process of raising the debt limit has at times engendered controversy, which occurred during the 2011 Debt Ceiling Crisis.

What could happen if Congress does not vote to raise the debt ceiling in 2023?

In a letter to the U.S. House of Representatives, U.S. Treasury Secretary Janet Yellen warned congressional leaders that the U.S. will reach its borrowing limit on Thursday, January 19. Yellen wrote that the Treasury will take “extraordinary measures” to avoid defaulting on its obligations, but she warned these measures might only be sufficient to cover obligations into June. Failure to meet the government’s obligations would cause irreparable harm to the U.S. economy, the livelihood of all Americans, and global financial stability, she warned. She also mentioned that the U.S. would risk facing another credit rating downgrade, similar to that of 2011.

Once the debt ceiling is reached, what spending will the Treasury cut?

In a letter to the U.S. House of Representatives, U.S. Treasury Secretary Janet Yellen warned congressional leaders that the Treasury will implement extraordinary measures to prevent the U.S. from defaulting on its obligations.

In January 2023, the Treasury will redeem existing and will suspend new investments of the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund. It will also suspend reinvestment of the Government Securities Investment Fund of the Federal Employees Retirement System Thrift Savings Plan.

Why did increasing the debt ceiling cause contentious debate in 2011?

Between 2008 and 2010, Congress raised the debt ceiling from $10.6 trillion to $14.3 trillion. In 2011, as the economy showed early signs of recovery and federal debt approached its limit again, negotiations began in Congress to decide spending priorities. Heated debate ensued between pro-debt politicians and fiscal conservatives. Pro-debt politicians argued that failing to raise the limit could result in late, partial, or missed payments to Social Security and Medicare recipients, government employees, and government contractors. Fiscal conservatives argued that any debt limit increase should come with limits on federal spending and debt accumulation.

The Bottom Line

Following the 2007-08 Financial Crisis, in an effort to slow down the severe recession as well as the persistently high unemployment rate, the government increased federal spending. As a result, the federal debt reached its limit on multiple occasions from 2008 to 2011 which led to a series of increases of the debt limit. In 2011, the Treasury asked for its borrowing capacity to be extended.

The 2011 U.S. Debt Ceiling Crisis was a contentious debate in Congress that occurred in July 2011 regarding the maximum amount of debt the federal government should be allowed. Congress resolved the debt ceiling crisis by passing the Budget Control Act of 2011, which became law on August 2, 2011. This act allowed the debt ceiling to be raised by $2.4 trillion in two phases, or installments.

An annualized total return is the geometric average amount of money earned by an investment each year over a given time period. The annualized return formula is calculated as a geometric average to show what an investor would earn over a period of time if the annual return was compounded.

An annualized total return provides only a snapshot of an investment’s performance and does not give investors any indication of its volatility or price fluctuations.

Key Takeaways

An annualized total return is the geometric average amount of money earned by an investment each year over a given time period.

The annualized return formula shows what an investor would earn over a period of time if the annual return was compounded.

Calculating the annualized rate of return needs only two variables: the returns for a given period and the time the investment was held.

Understanding Annualized Total Return

To understand annualized total return, we’ll compare the hypothetical performances of two mutual funds. Below is the annualized rate of return over a five-year period for the two funds:

Mutual Fund A Returns: 3%, 7%, 5%, 12%, and 1%

Mutual Fund B Returns: 4%, 6%, 5%, 6%, and 6.7%

Both mutual funds have an annualized rate of return of 5.5%, but Mutual Fund A is much more volatile. Its standard deviation is 4.2%, while Mutual Fund B’s standard deviation is only 1%. Even when analyzing an investment’s annualized return, it is important to review risk statistics.

Annualized Return Formula and Calculation

The formula to calculate annualized rate of return needs only two variables: the returns for a given period of time and the time the investment was held. The formula is:

For example, take the annual rates of returns of Mutual Fund A above. An analyst substitutes each of the “r” variables with the appropriate return, and “n” with the number of years the investment was held. In this case, five years. The annualized return of Mutual Fund A is calculated as:

An annualized return does not have to be limited to yearly returns. If an investor has a cumulative return for a given period, even if it is a specific number of days, an annualized performance figure can be calculated; however, the annual return formula must be slightly adjusted to:

For example, assume a mutual fund was held by an investor for 575 days and earned a cumulative return of 23.74%. The annualized rate of return would be:

Difference Between Annualized Return and Average Return

Calculations of simple averages only work when numbers are independent of each other. The annualized return is used because the amount of investment lost or gained in a given year is interdependent with the amount from the other years under consideration because of compounding.

For example, if a mutual fund manager loses half of her client’s money, she has to make a 100% return to break even. Using the more accurate annualized return also gives a clearer picture when comparing various mutual funds or the return of stocks that have traded over different time periods.

Reporting Annualized Return

According to the Global Investment Performance Standards (GIPS)—a set of standardized, industry-wide principles that guide the ethics of performance reporting—any investment that does not have a track record of at least 365 days cannot “ratchet up” its performance to be annualized.

Thus, if a fund has been operating for only six months and earned 5%, it is not allowed to say its annualized performance is approximately 10% since that is predicting future performance instead of stating facts from the past. In other words, calculating an annualized rate of return must be based on historical numbers.

How Is Annualized Total Return Calculated?

The annualized total return is a metric that captures the average annual performance of an investment or portfolio of investments. It is calculated as a geometric average, meaning that it captures the effects of compounding over time. The annualized total return is sometimes referred to as the compound annual growth rate (CAGR).

What Is the Difference Between an Annualized Total Return and an Average Return?

The key difference between the annualized total return and the average return is that the annualized total return captures the effects of compounding, whereas the average return does not.

For example, consider the case of an investment that loses 50% of its value in year 1 but has a 100% return in year 2. Simply averaging these two percentages would give you an average return of 25% per year. However, common sense would tell you that the investor in this scenario has actually broken even on their money (losing half its value in year one, then regaining that loss in year 2). This fact would be better captured by the annualized total return, which would be 0.00% in this instance.

What Is the Difference Between the Annualized Total Return and the Compound Annual Growth Rate (CAGR)

The annualized total return is conceptually the same as the CAGR, in that both formulas seek to capture the geometric return of an investment over time. The main difference between them is that the CAGR is often presented using only the beginning and ending values, whereas the annualized total return is typically calculated using the returns from several years. This, however, is more a matter of convention. In substance, the two measures are the same.

The Bottom Line

Annualized total return represents the geometric average amount that an investment has earned each year over a specific period. By calculating a geometric average, the annualized total return formula accounts for compounding when depicting the yearly earnings that the investment would generate over the holding period. While the metric provides a useful snapshot of an investment’s performance, it does not reveal volatility and price fluctuations.

An activist investor, typically a specialized hedge fund, buys a significant minority stake in a publicly traded company in order to change how it is run.

The activist investor’s goals may be as modest as advising company management or as ambitious as forcing the sale of the company, divestitures or restructuring, or replacing the board of directors.

Unlike private equity firms that buy and restructure companies in order to profit when they are resold, activist investors seldom acquire full or majority stakes. Instead, they use public communications and private discussions to win over other shareholders and company insiders. When such efforts fail, an activist investor may pursue a proxy contest to elect new directors in order to force the company to meet their demands.

Key Takeaways

Activist investors buy minority stakes in public companies to change how they are run.

If they fail to persuade company managers, they may wage a proxy fight for board seats.

Some hedge funds specialize in activist investing while institutional investors may engage in it from time to time.

Investor activism may focus on maximizing shareholder value or on the company’s social responsibilities.

The SEC has proposed tougher disclosure rules for activist investors that critics contend may make activism unprofitable.

Understanding Activist Investors

Activist investors are sometimes called shareholder activists, a term also used to describe those lobbying companies to improve working conditions for the overseas employees of their contractors, or backers of a dissident board slate elected to fight climate change.

However, many activist investor campaigns seek only to maximize shareholder value, and most of those are the work of hedge funds specializing in the unique mix of public pressure, behind-the-scenes lobbying, and business expertise required.

Unlike the public pension funds and mutual funds that also engage in activism at times, activist hedge funds may hold highly concentrated stakes and supplement them with additional leverage from derivatives like stock options to offset the considerable cost of such campaigns. In contrast with institutional investors that sometimes turn to activism after owning a disappointing investment for years, activist hedge funds typically buy a stake in an underperforming company shortly before calling for change, and hope to profit from the resulting turnaround and price appreciation.

In contrast to institutional investors, activist hedge funds are also more willing to use confrontational tactics, from poison-pen letters to management and unflattering public reports to proxy fights seeking to oust incumbent directors.

The rise of activist investors has been described as an effective market response to the agency problem, which arises when agents (in this case company managements) have the opportunity and the means to enrich themselves at the expense of clients (in this case shareholders—a diffuse group with limited powers to safeguard its ownership interests.)

How Activist Investors Make Their Case

Investor activists often announce their campaigns by filing a Schedule 13D form with the U.S. Securities and Exchange Commission (SEC), which must be filed within 10 calendar days of acquiring 5% or more of a company’s voting class shares.

Qualified institutional investors and passive investors, meaning those not trying to acquire or influence control of the company, may instead file a simplified Schedule 13G with less stringent disclosure requirements and thresholds. Schedule 13D filers must disclose, among other facts, their reasons for acquiring the stake and any plans they may have for the company in terms of mergers and acquisitions, asset disposals, capitalization or dividends, or other policies.

The initial 13D filing gives the activist investor a golden opportunity to publicize their case for change at the targeted company. At the same time, the filing curtails the activist’s ability to alter their stake in, and plans for, the company out of the public eye. Any changes to the facts disclosed on a Schedule 13D must be reported in an amended filing “promptly,” under current SEC rules.

Activist investors may use amended Schedule 13D filings to comment on a company’s response to their proposals. For example, when Netflix, Inc. (NFLX) adopted a poison pill after funds affiliated with Carl Icahn reported a stake of nearly 10% in the video streaming company, the funds filed an amended disclosure calling the poison pill “an example of poor corporate governance.” Activist investors may also write sharply worded letters to incumbent managers, issue press releases arguing their case to other shareholders, or privately lobby institutional investors to side with them.

Whichever tactics activist investors use must be persuasive, since the only way to overcome opposition from entrenched company management short of a hostile takeover is to persuade a sufficient number of other shareholders to replace the board in a proxy fight, or at least to be able to credibly threaten to do so.

The Future of Shareholder Activism

There has been a claim that “activism is dying,” lamented Carl Icahn in May 2022, contrasting the legendary investor’s few-holds-barred approach seen in the past. Some have feared the changes proposed to the Schedule 13D disclosure requirements in 2022 constitute a pressing threat, with Elliott Investment Management stating publicly that the proposed rules “will virtually shut down activism.”

In February 2022 the SEC had proposed shortening the initial Schedule 13 filing deadline from 10 calendar days to 5, with amendments due within a day of a material change rather than “promptly” as currently. The proposal, if passed, would effectively force 13D filers to specify holdings of derivatives (such as options) that confer an economic interest in the company without the shareholder rights associated with an outright stock position. Perhaps more controversially, the proposed rules would no longer require investors to agree to act in concert and be designated a single group by the SEC for Schedule 13D reporting purposes. Rules have also been proposed to make it harder for activist shareholders to squash a company’s environmental or other pro-ESG initiatives.

SEC Chair Gary Gensler argued the stepped up requirements proposed would address “an information asymmetry” between activist investors and other shareholders. Critics countered the proposed rules would make activism unprofitable by making it more difficult and costly for activist investors to accumulate significant stakes, while inhibiting communication among shareholders.

Despite these proposed rule changes, shareholder activism does not seem to be slowing down (at least, not yet). For example, activist investor Nelson Peltz reportedly made a profit of more than $150 million by acquiring shares of Disney (DIS) in November 2022, in a move that prompted a proxy fight against the returning CEO, Bob Iger; however, this brief fight was called off after Iger announced a restructuring plan that is expected to save the media giant $5.5 billion in costs and cut 7,000 employees. Peltz has expressed satisfaction with the company’s direction and decision to make changes, praising Iger and his management team. In early 2023, ValueAct Capital Management, a San Francisco-based activist hedge fund, took a stake in streaming media company Spotify Technology SA (SPOT), with the goal of cutting costs and streamlining management. ValueAct has also disclosed a major position and board seat in SalesForce (CRM), which now has no less than five large activist investor shareholders on board with long positions, resulting in early 2023 cost cutting measures that include layoffs of 10% of the company’s employees. In all three of the these examples, markets have reacted positively to the inclusion of activist shareholders, seeing their share prices afterwards outperform.

Do Activist Investors Ever Settle With Companies?

Yes, because activist investing is not a zero-sum game. Since activist investors and incumbent managers share an interest in the company’s success, they may sometimes agree to a mutually acceptable compromise. Such agreements typically grant the activist investor representation on the company board in exchange for a pledge to support management and the company’s director nominees for a specified time. The agreements may also specify steps management will take at activist investors’ behest, while including standstill provisions preventing the activist from increasing their stake in the company or requiring them to maintain a specified minimum stake.

Is Shareholder Activism Dying?

While some fear recently proposed SEC rule changes may put a damper on activist investing, it has not yet seemed to slow down. After taking a dip in 2020 and 2021 due to COVID19 restrictions, activist investors were seen back above 2019 levels. In fact, shareholder activism activity hit a record high in 2022. Some predict this upward trend will continue through 2023 and beyond despite regulatory roadblocks that may be put in the way, although only time will tell.

Do Activist Investors Create Value?

Activist investors have been effective at times in addressing the agency problem faced by shareholders whose interests don’t always coincide with those of entrenched management teams. They’ve certainly created value for themselves and other shareholders. Activist investing can’t easily be pigeonholed as good or bad, however. Activist investors look out for themselves and realize the lion’s share of the value they unlock. Their relatively short-term focus on strategies likely to lift the share price, such as return of capital to shareholders in the form of dividends or share buybacks, can prevent companies from making needed long-term investments.

Which Activist Investor Generates the Largest Share-Price Gains at the Outset?

It is difficult to know for sure which activist investors have been the more successful dollar-for-dollar and what other factors may cause particular stocks to rise in addition to an activist taking on a stake, but we can look to SEC disclosures and public statements made by these investors. Elliott Investment Management, for one, claims that its investments receive an average rise of 8% in the shares of the target company on the day the firm made its stake public. According to Elliot, its activist engagements have increased the market values of the targeted companies by an aggregate of more $30 billion.

Who Are the Biggest Activist Investors?

The largest activist shareholders by assets under management (AUM) as of Q1 2023 are listed in the table below, led by New York City-based Third Point Partners:

Largest Activist Investment Firms by AUM (Q1 2023)

Rank

Profile

Managed AUM

Region

1.

Third Point Partners

$18,1 billion

North America

2.

Pershing Square Capital Management

$16,8 billion

North America

3.

ValueAct Capital

$13,2 billion

North America

4.

Eminence Capital

$10,5 billion

North America

5.

Pentwater Capital Management

$9,9 billion

North America

6.

Starboard Value LP

$9,2 billion

North America

7.

Trian Fund Management

$7.6 billion

North America

8.

Effissimo Capital Management

$6,8 billion

Asia

9.

Sachem Head Capital Management

$6,2 billion

North America

10.

Scopia Capital Management

$2,7 billion

North America

Source: Sovereign Wealth Fund Institute (SWFI)

The Bottom Line

When activist investors use their significant but still relatively small minority stakes to push for change at publicly listed companies, they must often exercise their rights as shareholders to the fullest to get the attention of incumbent management and persuade other shareholders. Activists often call for extreme cost cutting measures, including layoffs, more streamlined management, and disposing of unprofitable units. The discipline they impose promotes shareholder-friendly policies at other companies as well. But they are not always right, and any public benefit they provide may be incidental to their pursuit of profits for themselves and their clients.