Daily Analysis 20241105

November 05th, 2024

Dow leads stocks lower as Wall Street braces for Election Day

US stocks slipped during a jittery session on Monday to kick off a week of potentially huge market-moving events — the presidential election and the Federal Reserve policy decision.

Dow…….41795 -257.6 -0.61%

Nasdaq. 18180 -59.93 -0.33%

S&P 500 5713 -16.1 -0.28%

FTSE…..8184 +7.1 +0.09%

Dax……19148 -107.1 -0.56%

CAC……7372 -37.4 -0.50%

Nikkei….38054 closed +0%

HSI………20568 +61.1 +0.30%

Shanghai.3310 +38.2 +1.17%

IDX…7479.50 -25.76 -0.34%

LQ45…913.42 +0.81 +0.09%

IDX30.470.71 +1.26 +0.26%

IDXEnergy….2717.76 -12.16 -0.45%

IDX BscMat1379.00 -21.60 -1.54%

IDX Indstrl..1090.32 -5.19 -0.47%

IDXNONCYC.748.63 +0.67 +0.09%

IDX Hlthcare1506.68 -15.60 -1.02%

IDXCYCLC…..868.43 -12.36 -1.40%

IDX Techno..3953.41 -49.09 -1.23%

IDX Transp 1445.59 -33.07 -2.24%

IDX Infrast 1472.57 -13.45 -1.23%

IDX Finance1512.89 -3.39 -0.22%

IDX Banking1292.34 +6.27. +0.49%

IDX Property..821 -12.6 -1.51%

Indo10Yr.6.8735❗️+0.0034 +0.49%

ICBI….392.7677❗️-0.0785 -0.02%

US2Yr.4.168 ❗️-0.044 -1.04%

US5Yr 4.148 ❗️-0.007 -0.17%

US10Yr4.293❗️ -0.093 -2.12%

US30Yr.4.466❗️-0.115 -2.51%

VIX..21.98 +0.10 +0.46%

USDIndx 103.8860❗️-0.400 -0.38%

Como Indx.282.75 +3.31 +1.18%

BCOMIN…..149.10 +0.69 +0.47%

IndoCDS..71.24 +1.01 +0.01%

(5-yr INOCD5) (01/11)

IDR…….15752.00‼️ +20.50 +0.13%

Jisdor..15723.00‼️ +28.00 +0.18%

Euro…1.0878❗️ +0.0006 +0.06%

TLKM.17.70 +0.21 +1.17%

( 2783)

EIDO…21.16 +0.08 +0.38%

EEM……44.74 +0.20 +0.45%

Oil………71.47 +1.98 +2.85%

(WTI,Nymex)

Oil………75.21 +2.10 +2.89%

(Brent)

Gold…2746.20 -3.00 -0.2l11%

(Comex)

Gold…2736.72 +0.19 +0.01%

(Spot/XAUUSD)

Timah.31724.00 +511.00 +1.64%

(Closed 01/11)

Nickel.16120.50 +136.50 +0.85%

(Closed 04/12)

Silver….32.6 -0.07 -0.21%

Copper.443.15 +6.00 +1.37%

Iron Ore 62% 102.49 -1.29 -1.24%

(01/11)

Nturl Gas 2.789 +0.126 +4.73%

Ammonia China 2766.67 +46.67 +1.72%

(Domestic Price)(04/11)

Coal price.143.90 -0.05 -0.03%

(Nov/Newcastle)

Coal price.144.90 -0.05 -0.03%

(Dec/Newcastle)

Coal price.145.90 +0.20 +0.14%

(Jan/Newcastle)

Coal price.146.70 +0.20 +0.14%

(Feb/Newcastle)

Coal price.119.05 +0.65 +0.55%

(Nov/Rotterdam)

Coal price.119.20 +0.10 +0.21%

(Dec/Rotterdam)

Coal price.120.20 +0.30 +0.25%

(Jan/Rotterdam)

Coal Price 120.45 +0.20. +0.17%

(Feb/Rotterdam)

CPO(Jan) 4891 +26 +0.53%

(Source: bursamalaysia.com)

Corn………416.50 +2.00 +0.48%

SoybeanOil 45.56 -0.74 -1.60%

Wheat……568.75 +0.75. +0.13%

Wood pulp.4640.00 unch +0%

(Closed 04/11)

©️Phintraco Sekuritas

Broker Code: AT

Desy Erawati/ DE

Source: Be loomberg, Investing, IBPA, CNBC, Bursa Malaysia

Copyright: Phintraco Sekuritas

US merah, europe merah, asia ijo, IHSG yang merah dalem, US Treasury bond merah dalem, kayanya technical rebound dulu hari ini mah IHSG, tapi ga banyak

USD index down, gold spot ijo tipis, tin nickel copper ijo, silver iron ore merah, perlu dicermati TINS dan INCO, oil ijo tebel, gas juga, coal melempem, CPO naik lagi, kita liat AKRA dan AALI LSIP

IHSG – nah ini mulai FNB, ada titik terang, stoch macd rsi mfi w% masih jelek semua, kalo ini wave 4 masih agak dalem, tapi sah aja berhenti sekarang juga, ABC nya cenderung flat. Kita cermati BBCA BBRI

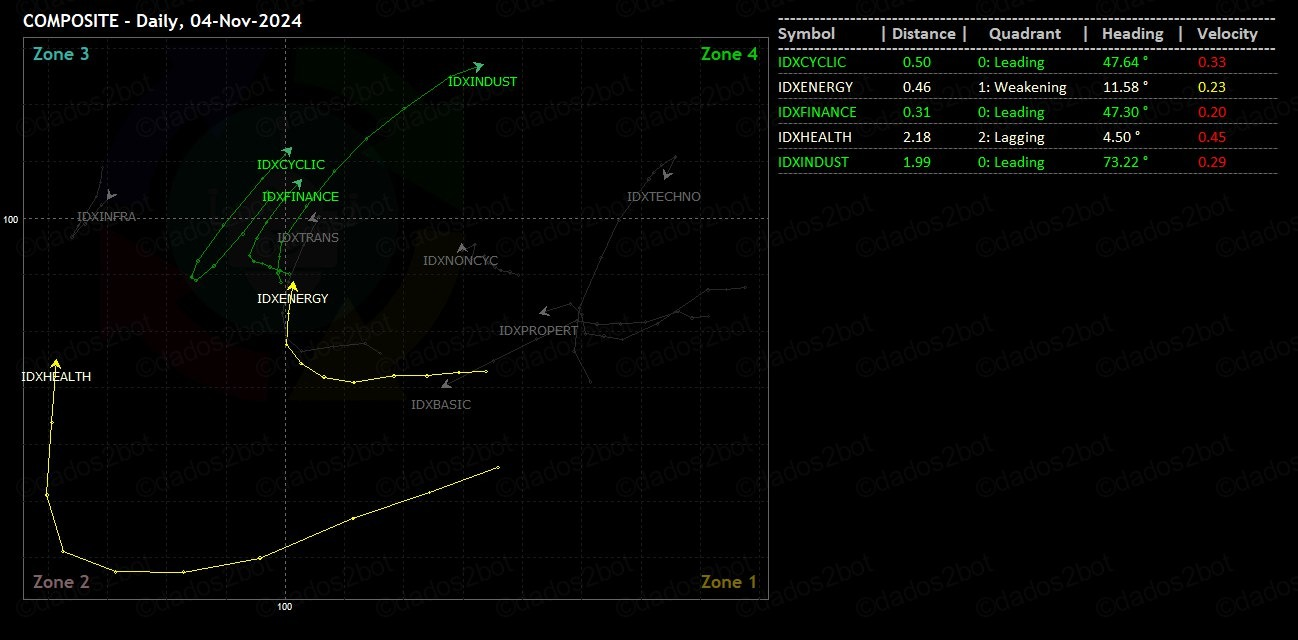

Industrials, Consumer Cyclicals, Financials, nah ini kalo bener jalan index ikut… Energy sama healthcare siap2, infrstructure belum jadi jalan, JSMR terpaksa cutloss kemaren

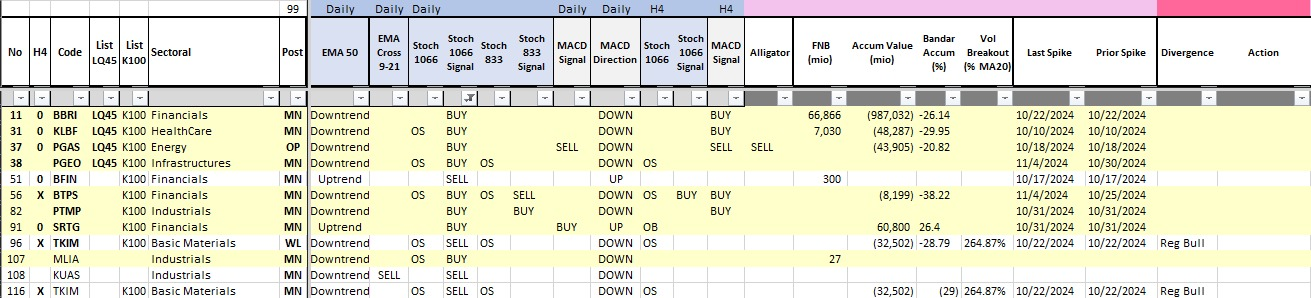

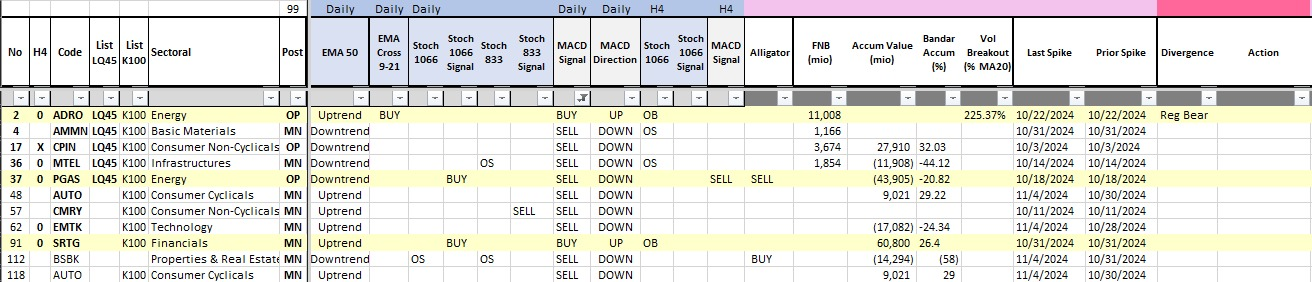

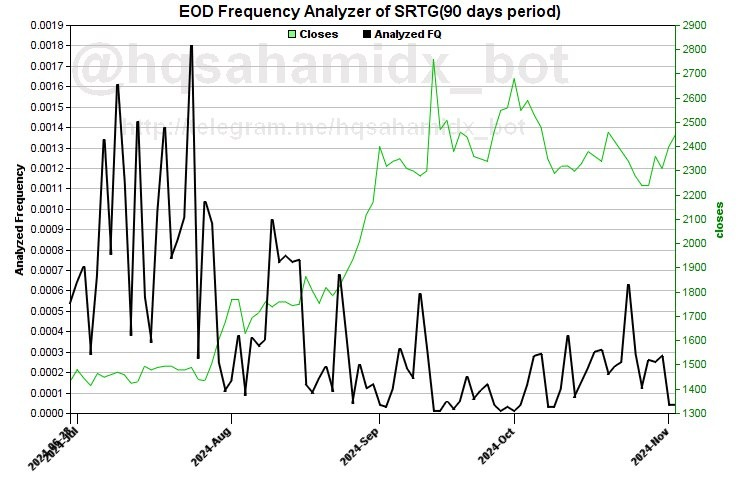

Stochastic Buy Signal: BBRI KLBF PGAS PGEO BTPS PTMP SRTG MLIA, SRTG big accum

MACD Buy Signal ADRO SRTG

![]()

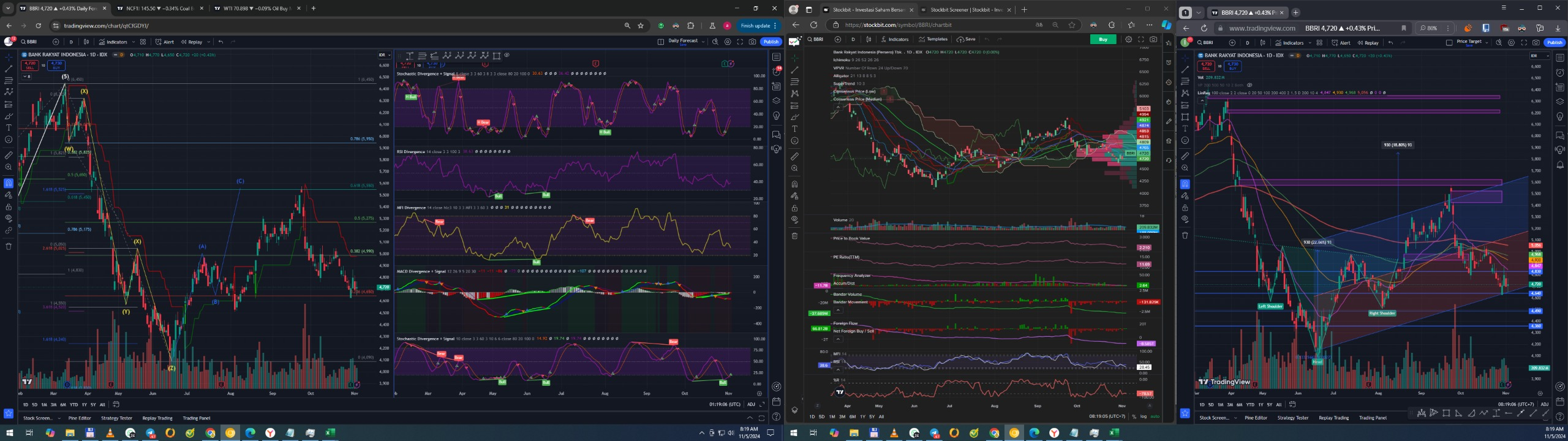

BBRI – stoch buy, MACD dikit lagi, MFI masih down, w% sw, BD masih dist, FF rev acc, ini bisa spec buy harusnya, bisa jadi hari ini start gerak

Big caps emang jarang spike, ini ada tapi kecil

Average aman, BD lagi pada diem, tunggu momentum aja ini, tapi BBRI seringkali kebaca di Stoch dan digerakin juga sama foreign, so Spec Buy BBRI at last close price, setengah botol dulu

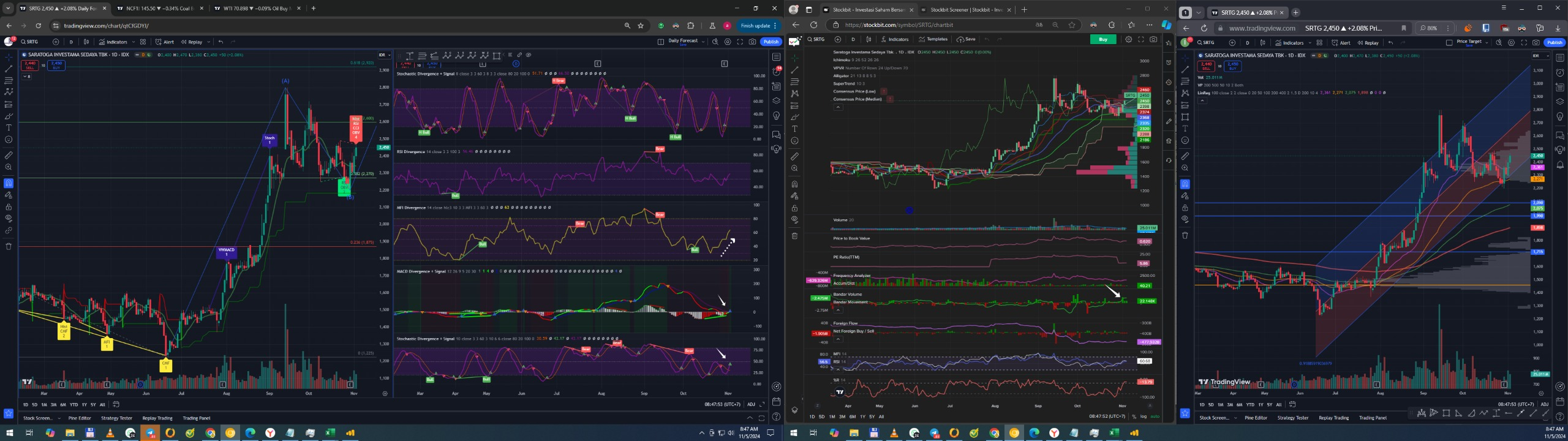

SRTG – stoch MACD buy, MFI up, w% uptrend, tembus ke atas cloud ichimoku, alligatornya nyusun buy lagi, BD accum, FNS tapi, dari retracement pattern udah nyusun 50-38 mau ke 61. Agak resiko di index yang belum pasti jalan lagi wave 5, tapi faktor pendukung buy nya udah ok, BOW SRTG di tengah candle kemaren, setengah botol aja harusnya ok ini

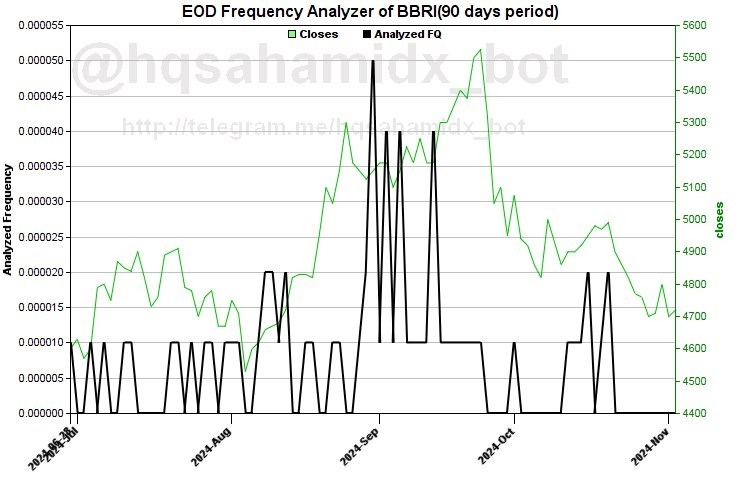

spike kecil, spike gede sebelumnya belum done, masih mungkin dikejar sih ini

![]()

Average nya ga aman, amannya minimal buy di bawah average BB di 2335, so jangan FOMO, BOW 2330 aja deh setengah botol

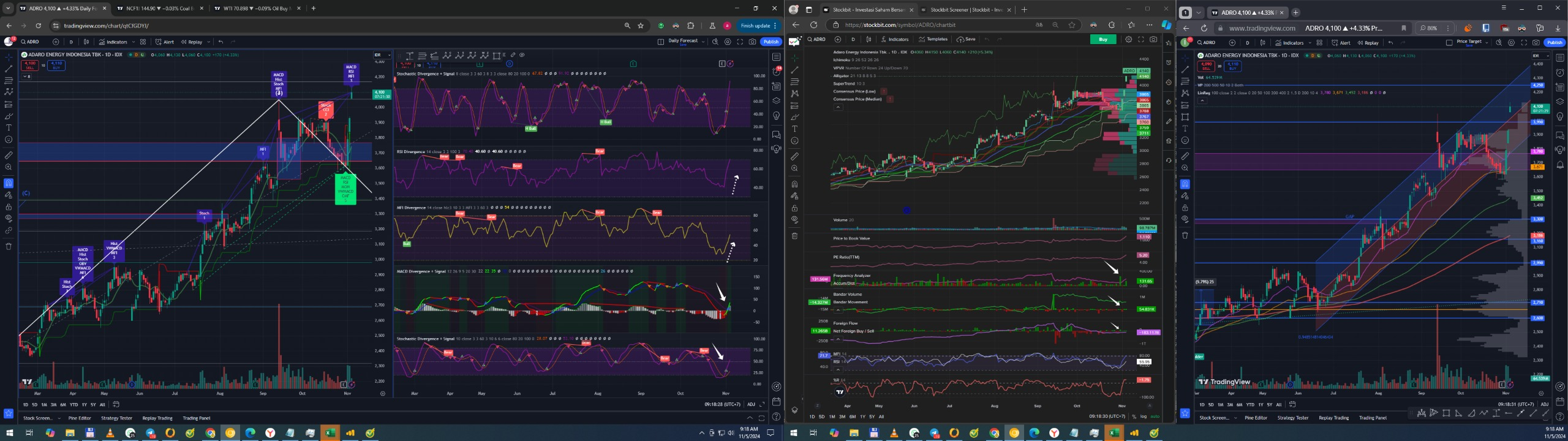

ADRO – ada yang aneh ini, hajatan sendiri… stoch macd buy MFI up, BD FF acc, loncat2 pake bikin gap segala, padahal coal price nya melempem… Ga berani ngejar, kalo energy jalan juga masuk di ITMG aja sama INDY yang ketinggalan

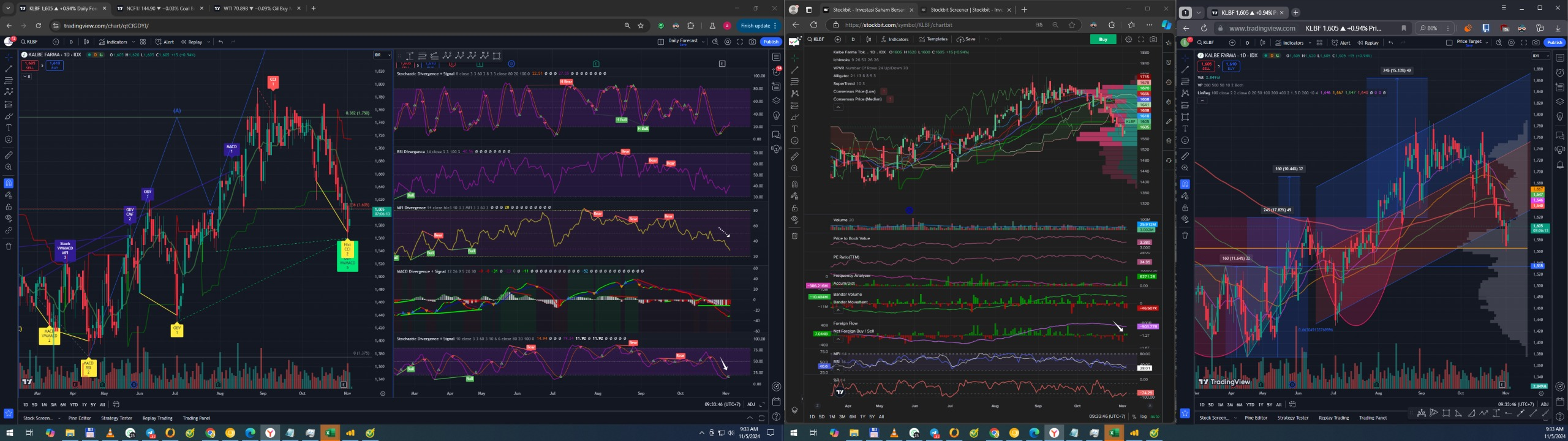

KLBF – sedikit overpriced, masih ok lah buat trade, stoch buy macd belum ada reg bull div, MFI masih down, w% mulai up, BD dist, FNS, masuk watchlist dulu, retracement pattern sih harusnya bawa mantul dari fibo 23

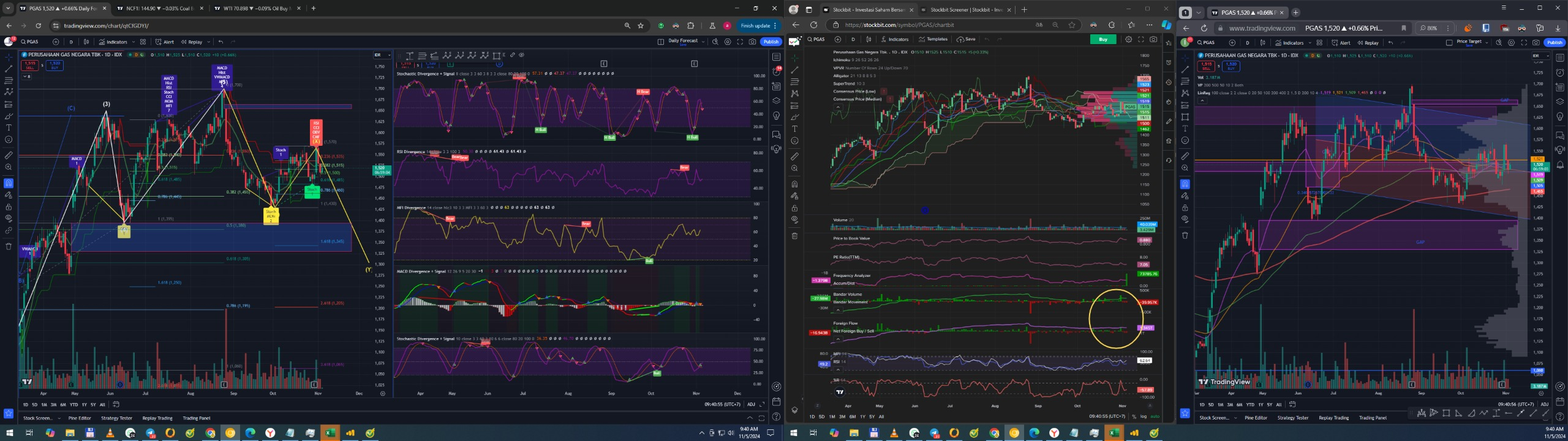

PGAS – belum saatnya